Surface Tension

loods rarely arrive the same way twice. Some are driven by hurricane-induced storm surge that pushes seawater inland block by block. Hurricane Harvey behaved differently, hovering over the Gulf Coast for days and dropping feet of rain on Houston. Sometimes a river slowly exceeds its banks after days of steady upstream rain, and sometimes it rises with extraordinary speed after heavy localized rain, as was seen in the tragic Kerr County, Texas, event in 2025. And increasingly, it’s none of those things; instead, we’ve seen intense cloudbursts overwhelm streets, basements, and storm drains in places that don’t think of themselves “flood-prone” at all.

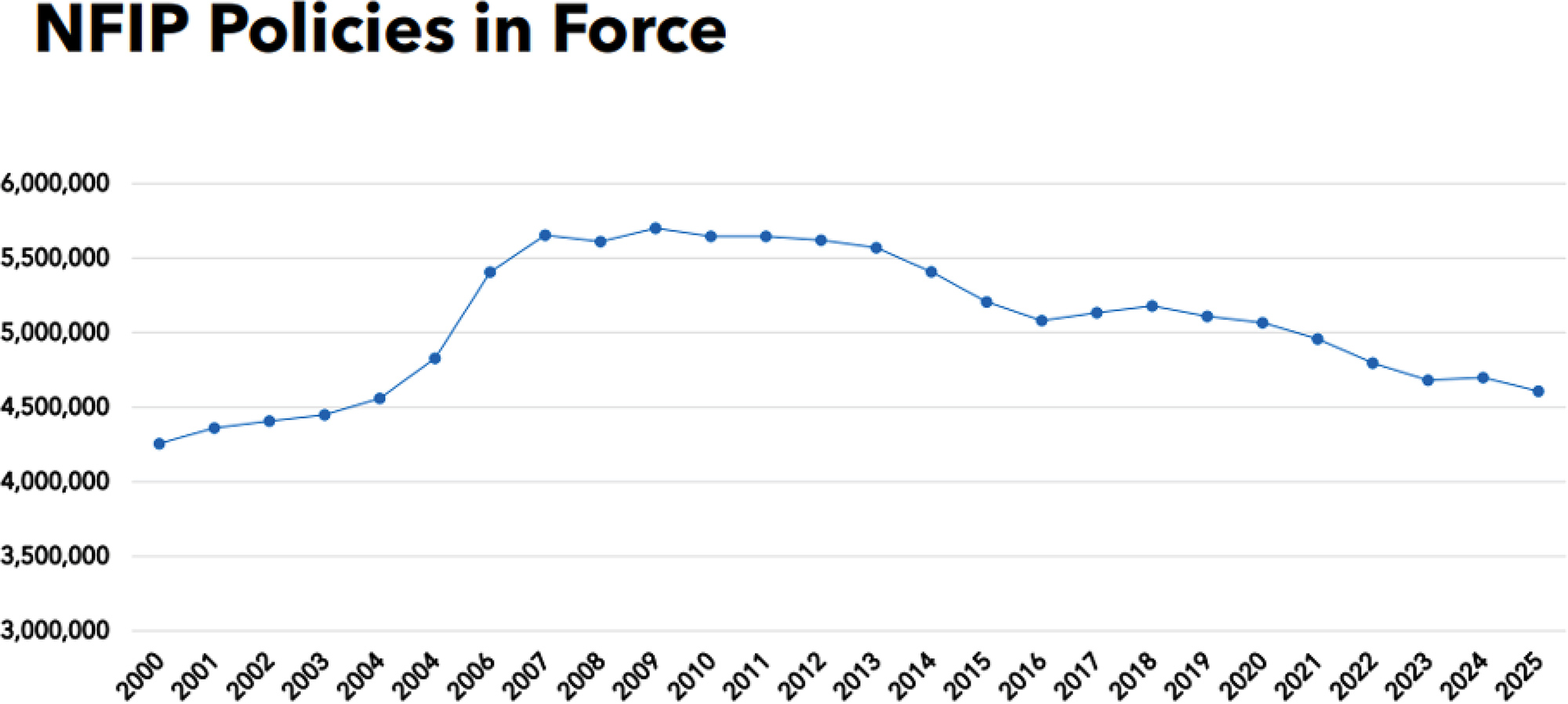

Insurance coverage has failed to keep pace with this growing risk. Most households affected by inland or urban flooding still have no flood insurance at all, even after experiencing losses firsthand. This coverage gap is no longer a mystery of modeling. Flood risk today is better measured, more granular, and more legible than at any point in the past; both public and private actors can estimate property-level exposure with a degree of confidence that would have been unthinkable a generation ago, and modeling breakthroughs continue to accelerate. And yet uptake remains stubbornly low, especially outside the narrow slice of properties where coverage is mandatory.

That tension — between rising, increasingly visible flood risk and persistently limited insurance coverage — is the starting point for this article. Private flood insurance has finally become viable, supported by new models, new capital, and new regulatory pathways that barely existed a decade ago. But viability is not the same as reach. Without changes to how flood insurance is distributed, incentivized, and embedded into household decision-making, private flood will remain a niche solution: well designed and technically impressive, but still absent when people need it the most.

“Flood” is not just one peril

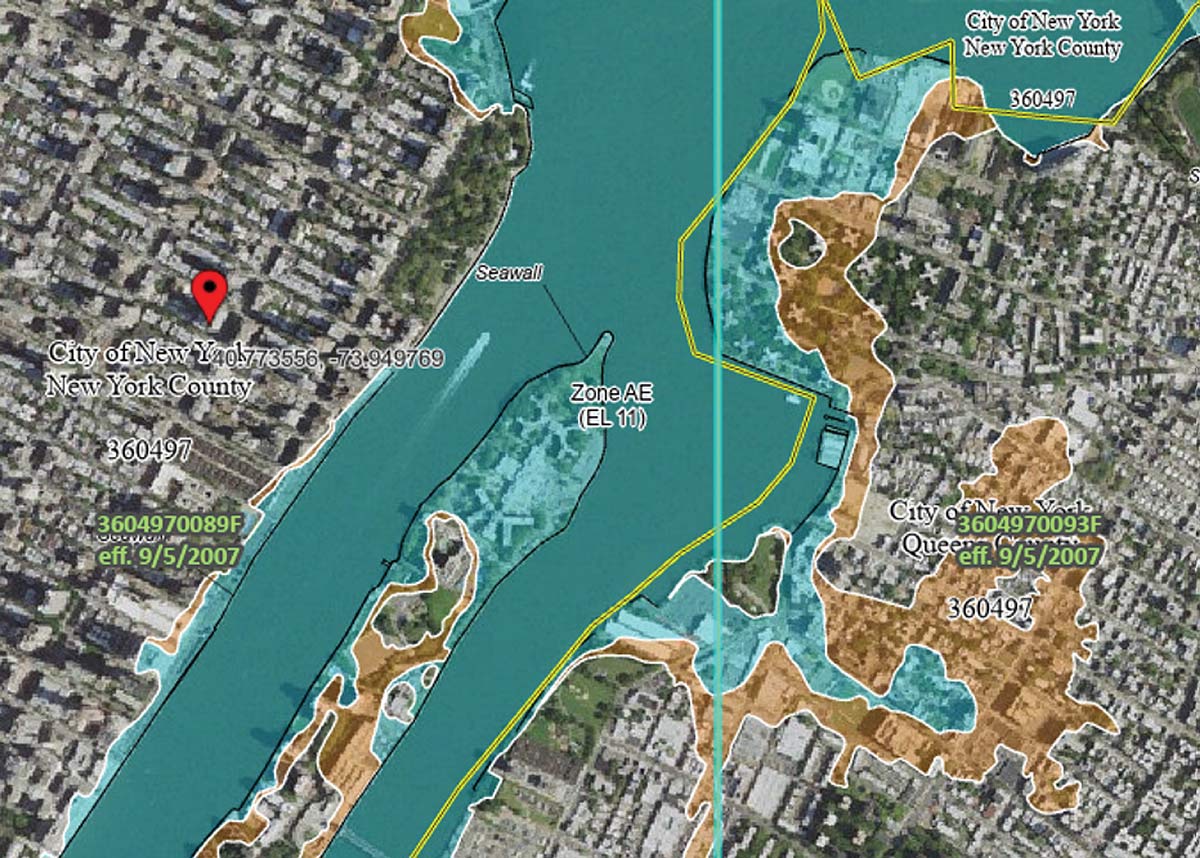

Coastal storm surge is the version of flood risk most people picture most readily. It is driven by wind pressure pushing seawater inland. Losses tend to track familiar geographies: barrier islands and low-lying coastal plains. The footprint can be large, but the risk is legible — people know they live “near the water.”

Fluvial (riverine) flooding is less intuitive because it is a system problem. A property can flood because of rainfall miles away, hours or days earlier, interacting with soil saturation, upstream development, and watershed geometry. River floods also span a spectrum: some are slow and forecastable, while others behave like flash floods when intense rain falls over a narrow area and channels fill faster than warnings can travel, trapping communities.

These differences make flood risk patchy and, in many places, invisible. Public understanding and many institutional triggers still anchor on binary categories, like being inside or outside of a Special Flood Hazard Area (SFHA), defined as having a greater than 1% annual chance of flooding. But much of today’s damaging flood experience does not respect those boundaries. The consequence is a persistent mismatch: households and mortgage lenders often treat flood as a niche coastal or river-adjacent concern, while losses increasingly reflect a wider set of mechanisms and geographies. That disconnect helps explain why flood insurance institutions have struggled to adapt.

How flood became a federal problem

This retreat coincided with a shift in how flood losses were handled politically. Large floods increasingly triggered federal disaster aid, infrastructure spending, and emergency relief. That response helped communities recover, but it also weakened the case for voluntary insurance. Flood risk, in practice, became socialized ex post rather than pooled ex ante, and this continues to be the case today.

The modern framework took shape in 1968 with the creation of the National Flood Insurance Program (NFIP). The NFIP was not designed simply to replace private insurance. It was built around a dual mandate that remains central to its identity. First, it aimed to make flood insurance broadly available in places where private markets would not operate. Second, it sought to reduce future flood losses by tying insurance availability to community floodplain mapping, land-use controls, and mitigation standards adopted by local governments.

The program’s delivery mechanism reflected this hybrid role. Under the “Write-Your-Own” (WYO) structure, private insurers sell and service NFIP policies under their own brands, while the federal government retains the underwriting risk and sets rates and terms. The arrangement leveraged private distribution and claims infrastructure without requiring insurers to put capital at risk. That structure has long created incentive frictions: flood is an administrative line rather than a strategic one, offering limited upside for insurers or agents, little reward for risk reduction, and few reasons to actively promote coverage outside mandatory purchase scenarios.

From the outset, the NFIP was asked to balance competing goals that would be difficult for any institution to reconcile. It was expected to be financially sound, politically palatable, widely available, and supportive of long-term risk reduction — all while operating in places where flood risk was highest and mitigation most expensive. That tension has shaped the program ever since, and it continues to influence how flood insurance is perceived today.

The NFIP today

The most visible expression of that shift is Risk Rating 2.0, FEMA’s overhaul of how flood risk is priced. Rather than relying primarily on broad flood zones and elevation thresholds, the updated framework incorporates multiple catastrophe models, property-level characteristics, and a wider set of flood risk drivers. The result is a rating system that produces far more differentiated premiums and aligns more closely with expected loss than its predecessors ever could.

Importantly, the NFIP’s modernization did not rely on a single model or vendor. The NFIP now blends multiple model views, empirical loss data, and portfolio considerations in ways that resemble best practices in the private market. Evans notes that while the NFIP has guardrails, “within the constraints it has it is now a pretty sophisticated pricing approach.”

Those constraints, however, remain substantial. Rates are subject to statutory caps and glide paths that limit how quickly premiums can adjust, even when updated risk signals point sharply upward. Coverage limits of $250,000 for residential and $500,000 for commercial are increasingly inadequate relative to replacement costs in many markets. In addition, the requirement for mandatory purchase of flood insurance is still tied to SFHAs, anchoring participation to legacy flood maps even as a growing share of losses occurs outside those zones. The result is a program that can assess risk with increasing clarity but cannot fully act on that information.

Private flood reemerges

Computing power eventually caught up. Katz describes how, by the early 2010s, “computers were finally getting fast enough that you could start to do this nationally and give carriers confidence in the results.” At the same time, data inputs improved dramatically. High-resolution elevation data, land-use and land-cover datasets, and better precipitation modeling allowed modelers to approximate surface runoff, ponding, and drainage behavior in ways that had previously been infeasible.

Those improvements mattered most outside traditional floodplains. In many areas classified as low risk under FEMA’s mapping regime, pluvial flooding dominated loss experience. Cities like Atlanta — where Katz notes there is no major river running through the city — were systematically underestimated, despite topography and development patterns that funnel water into vulnerable areas.

Equally important was the ability to translate model output into underwriting signals insurers could actually use. As Katz puts it, the breakthrough was not just better hazard science, but the ability to run models consistently, compare results across vendors, and integrate them into rating and underwriting workflows. Once that became possible, flood stopped being an unquantifiable tail risk and became something insurers could segment, price, and manage.

Regulatory changes removed the next barrier. When private flood policies were allowed to satisfy mandatory purchase requirements for federally backed mortgages, the market shifted from theoretical to viable. Without that recognition, private flood could only function as an excess or voluntary product. With it, insurers could compete directly for primary coverage, particularly for properties where NFIP pricing or coverage limits no longer aligned with perceived risk.

Capital followed these capabilities. As modeling improved, reinsurers grew more comfortable deploying capacity to flood programs — often with close scrutiny of accumulation management and underwriting discipline. A new ecosystem of MGAs, specialty carriers, and reinsurance-backed programs was thus able to grow.

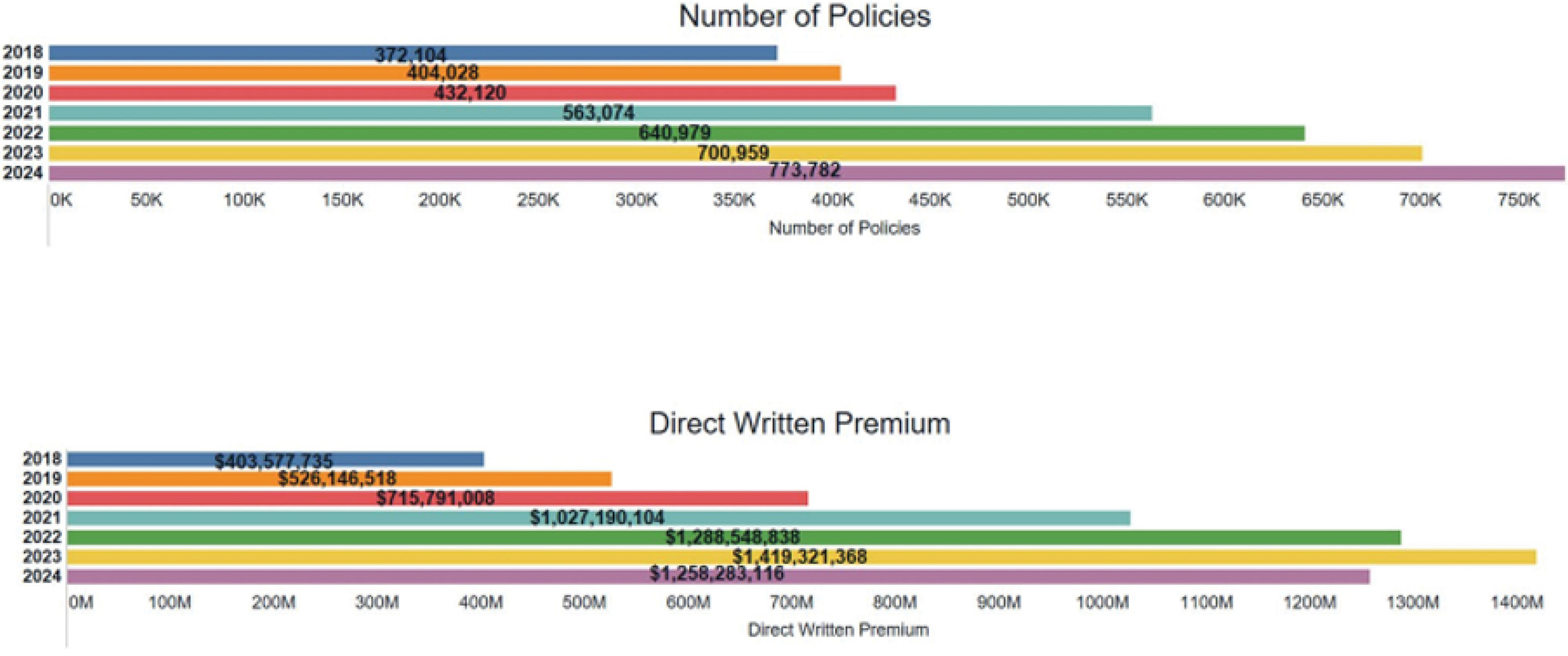

The private flood market that has emerged over the past decade is no longer hypothetical. A recognizable set of players and business models now demonstrates that flood insurance can be written, priced, and supported at scale. What the market has not yet demonstrated is how to translate that technical viability into broad adoption.

At the center of the market are specialist MGAs that have made flood their primary focus. Neptune Flood is the most prominent example, having built a national primary flood product that competes directly with the NFIP in many regions. Neptune’s growth — and its headline-grabbing 2025 IPO — validated the basic proposition that private flood could operate beyond narrow excess layers.

Reinsurers, meanwhile, have moved beyond passive capital provision. Firms like Swiss Re have developed increasingly integrated flood solutions for primary carriers and MGAs, combining modeling, pricing support, accumulation management, and quota share capacity. But as Evans emphasizes, the goal is not to make flood permanently “risk-free” for insurers. “Some companies see the value in flood but don’t want it on their balance sheet yet,” he noted. “If flood is going to become common, some insurers are going to have to retain the risk over time.”

In practice, that often means heavy quota share structures early on, paired with an expectation that insurers will gradually take on more exposure as confidence builds. “There isn’t a lack of flood capital,” Evans observed. “There’s a lack of insurers willing to make this a priority.” End-to-end reinsurance solutions can lower barriers to entry, but they cannot substitute for carrier commitment.

Despite this activity, the shape of growth remains telling. Much of the private flood market has expanded by serving risks that are already relatively well understood and economically attractive, such as homes exceeding NFIP coverage limits, properties near mapped floodplains, or policyholders reacting to premium increases. In many cases, private policies substitute for NFIP coverage rather than materially expanding the number of households insured. That dynamic was especially visible following Risk Rating 2.0, when pricing dislocations temporarily accelerated private-market growth before trends normalized.

The challenge facing private flood insurers today is therefore not underwriting or capital. Those problems are largely solved. The harder problem is scale — making flood insurance a routine purchase rather than a reactive one. That requires solving distribution: bringing coverage to the point of sale, aligning agent incentives, and rewarding market expansion rather than selective participation. The private flood sector will remain limited if it is built primarily on cherry-picking around the NFIP or grabbing growth when NFIP funding halts, as it did during the recent 2025 federal government shutdown. One that succeeds in broadening participation could begin to close the persistent gap between flood risk and flood coverage.

Flood insurance at the confluence

The NFIP was never meant to operate as a purely commercial insurer. Its mandate extends beyond risk transfer and into floodplain management, mitigation standards, and land-use signaling — an explicitly political choice to sustain communities in flood-prone areas. Private flood markets, by contrast, are built to price and select risk, not to regulate development or preserve broad access to coverage. Without a public backstop, underwriting and pricing would render large parts of the country effectively uninsurable. The result is that the NFIP and private flood are complementary rather than competing substitutes. The former provides baseline availability and policy structure, while the latter offers flexibility and capacity where underwriting confidence is strongest. The danger lies not in overlap, but in imbalance — where private insurers concentrate on economically attractive risks, while the NFIP increasingly absorbs the most difficult ones.

The U.S. flood insurance system is now approaching a genuine inflection point. The technical barriers that once constrained both public and private markets have largely fallen away. Risk is better measured, capital is available, and multiple operating models have proven viable. What remains unresolved are institutional choices about distribution, mandates, and risk sharing that will determine what kind of market ultimately emerges.

Broadly speaking, there are only a few plausible paths forward. One is continued drift: private flood grows largely through substitution, while the NFIP increasingly absorbs the most difficult risks and functions as a deeper residual market. Another is market-led expansion, in which bundling, embedded distribution, and carrier commitment make flood insurance routine in low- and moderate-risk areas, with the NFIP remaining central but less dominant. A third, more politically challenging path would involve changes to mandatory purchase or disclosure regimes that more explicitly treat flood as a shared household risk rather than an optional add-on.

None of these outcomes is preordained. But the direction taken will depend less on further modeling breakthroughs than on whether insurers, regulators, and policymakers can align around expanding participation rather than merely reallocating existing demand.

Regulators are already responding to this transition. State insurance departments and national bodies like NAIC have increased their attention, focusing on consumer clarity, solvency, accumulation risk, and model governance as more flood exposure moves outside the NFIP’s direct purview. The aim is not to slow innovation, but to place guardrails around a market that is still finding its footing.

Even with better oversight and better products, however, the central challenge remains unresolved: flood insurance is still treated as optional. It is rarely bundled with homeowners coverage, rarely presented clearly at the point of sale, and rarely revisited absent a lender mandate or recent loss. Mandatory purchase requirements, narrowly tied to SFHAs, capture only a fraction of today’s risk. Outside those zones, participation depends on individual initiative, an approach that has repeatedly failed to produce meaningful risk pooling. Until flood is treated as a core household risk rather than a specialty add-on, uninsured losses will continue to be borne largely by homeowners themselves.

Sources

- Congressional Research Service, Private Flood Insurance and the National Flood Insurance Program.

- NFIP’s Pricing Approach.

- NAIC 2025 Fall National Meeting Climate and Resiliency (EX) Task Force Meeting Slides.

- Jencap Flood Insurance Trends Approaching 2026.

- Insurance Information Institute, Spotlight on: Flood Insurance.