tepping forward into the wake of COVID red ink in personal auto, now awash in profitability (like the green Chicago River), we witnessed some true innovation coming from data heavyweight champion CarFax and humble analytic superhero consulting actuarial firm Pinnacle Actuarial Resources. The complexity, structure, and depth of their new model is a true example of innovation matched only by the thoughtfulness of their approach to communicating what’s new and improved to departments of insurance and their experts.

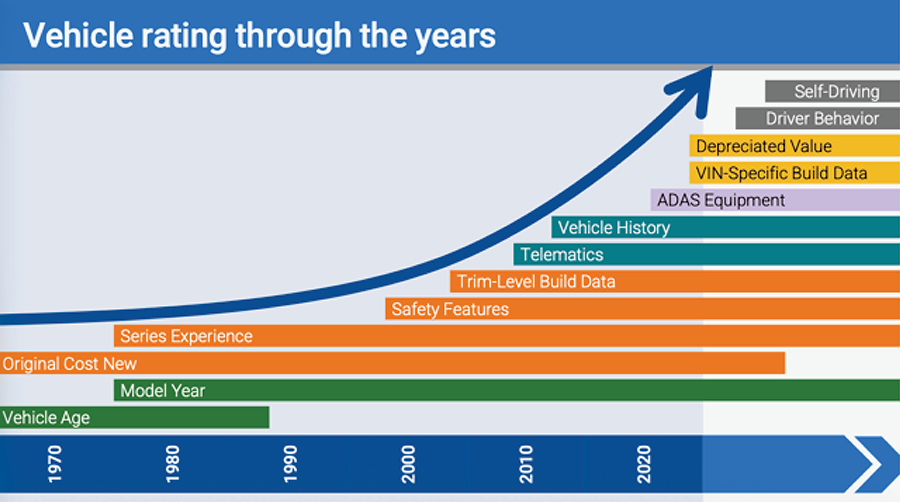

Donald Hendriks, ACAS, ASA, FCA, MAAA, director of analytics, CARFAX Banking & Insurance Group, and Joe Griffin, ACAS, senior consulting actuary, Pinnacle Actuarial Resources, demonstrated the challenges of developing a filing strategy as well as a technical communication strategy to introduce the “newer” nonparametric models to departments of insurance still using the “new” parametric model evaluation methods of the predictive modeling revolution from 20 years ago.

The GBM over GLM differences and similarities were a main attraction at several other sessions during the Ratemaking, Product, and Modeling seminar (RPM), but Hendricks and Griffin were able to share current examples of how storytelling to regulators is making solid headway, or not.

Market profitability in personal auto from 2019 to now has seen a swing from the worst performance in the millennia to the best in just a five-year period. Indeed, while much of that improvement was brute force base rate hiking, what comes next for competition is more accurate pricing in a value at risk volatile market like no current practicing actuary has ever seen. Here is where their innovation shines.

Hendriks demonstrated how vehicle value at risk has levitated above historical relativities. This is further compounded as it intersects and interacts with the most insurance-friendly vehicle feature innovations and safety (such as automated driver assistance), which have just entered the vehicle in operation fleet at scale in the last 10 years or so. The fitment of a variety of technologies onto a “go forward” set of vehicles was a key point in why different tech on different vehicles at different times creates more complexity than traditional models can deal with effectively.

He also showed how the lingering effects of COVID are creating a longer and higher demand for used vehicles, which is compounding the inaccurate MSRP problem across many additional years as depreciation is less for both the $50k version and the $70k one. This hidden truth can compound claim statistics as higher vehicle values can support higher claim repairs and still clear the total loss thresholds used across the industry.

Griffin and Hendriks demonstrated that modeling method stalwart GLM is less fit for use nowadays as both the spread in complexity of features and heterogeneity of values at risk leave underfitting inaccuracies compared with GBM approaches. The comparison of lift showed dramatic improvement in how the GBM methods were able to segment things like older and newer features and multiple technologies installed versus not installed.

While Griffin and Hendriks showed how their first big step in using vehicle value in rating makes sense, they also demonstrated that there is more work to be done to address varying depreciation by both vehicle type, make, model, and vehicle age. While a pre-COVID-to-now slide showed how unprepared prior pricing models were for this type of value at risk retained value problem, there was no discussion on what bumps in the road may lie ahead (tariffs, innovation, war, oil supply, etc.).

They outlined the technical and communication challenges they are facing with filing their models for use in pricing. Examples are predictor importance plots, lift metrics, SHAP values and “beeswarm” plots, and strongly structured filings with deep documentation (from the older 70-page GLM supports to about a 500-page Vehicle Build Score modeling package with a 270-page base and 200 pages of backup materials).

Dealing with the heterogeneous technologies and volatile depreciation swings across years, models, and features means the newer model methods are required. And newer ways of interacting with regulators are needed too.

As Hendriks said, “filing a GBM is new and we are overcoming skepticism. Regulators want competition and innovation in their states but need explainable models — like they did 20 and 30 years ago with GLM models, including by peril and by coverage.”

In summary, consumers want cars with innovations and insurers are hard at work understanding the relative risk of these higher priced options, feature-rich models, and a used car market that is rising above all experience.