Cost Drivers and Affordability in Personal Automobile Insurance

he CAS Spring Meeting session, “Cost Drivers and Affordability in Personal Automobile Insurance,” addressed one of the biggest headlines of the year in the popular press — affordability of insurance — with an emphasis on the most relatable kind to a consumer: a personal auto policy. Susan Kent, FCAS, MAAA, MS, described traditional affordability metrics and then discussed how, where, and how much stress was being seen in the current market. Margo Mackenzie, FCAS, MAAA, covered contributing factors in the cost driver universe. Finally, Jared Smolik, FCAS, CERA, reviewed what companies and states are trying to do about it now, with a key focus on state-level interventions that appear to be working.

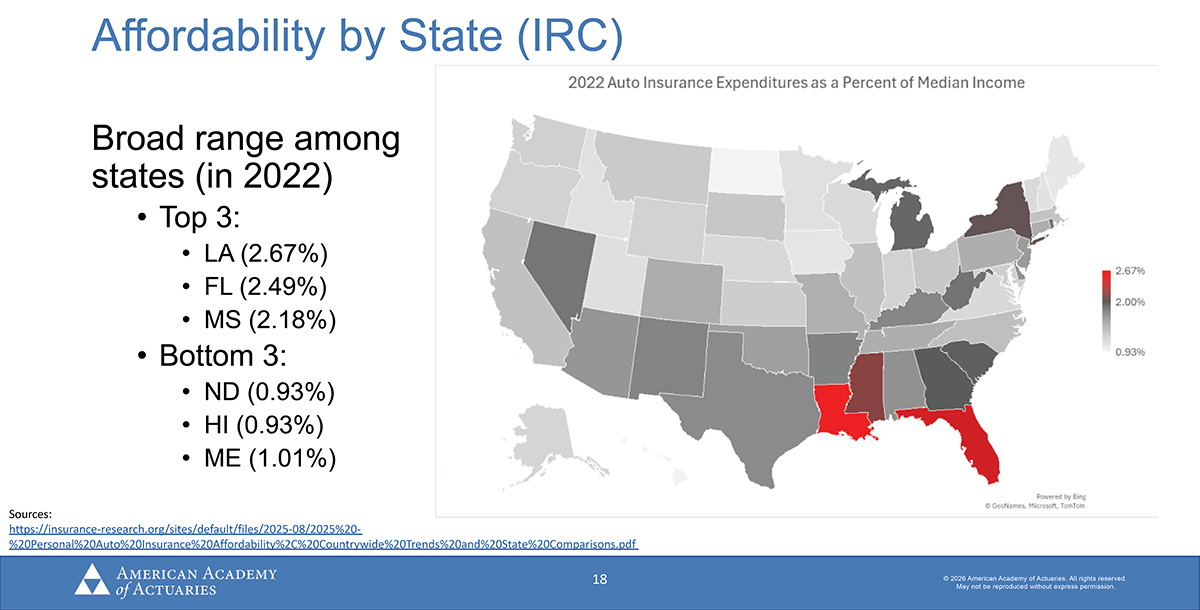

Kent opened the session by covering how auto insurance affordability has become an increasing concern as claim costs and insurance costs have risen. When insurance costs rise faster than household incomes, the budgetary stress at household levels creates more pressure on everyone involved. One measure of that has been more consumers shopping for insurance. This same pressure is evidenced on most other lines of business, she noted.

Kent explained that there are a lot of affordability issues that don’t make the headlines as well. One of these issues is that personal lines auto insurance, as a compulsory cover, can create pressure to raise the incidence rate of uninsured and underinsured drivers and claims. Costs are what they are, so companies are having to deal with increased churn and unstable customer retention They are seeing increases in nonstandard coverage, drops of full coverage, and larger comprehensive and collision deductibles as households seek to lower auto insurance premium payments while assuming more risk.

Kent said that a person in Manhattan (where the meeting was held) may not need a car, but in her hometown in Ohio, a vehicle was a necessity for daily mobility needs. This financial pressure on an everyday necessity creates tension between consumers and regulators and heightens the risk of fraud, Kent explained.

She noted that the history of COVID-19 showed less driving, resulting in premium givebacks, but then rates escalated dramatically, pushing rates to levels higher than the threshold. The current concerns over potential impacts of tariffs and observably higher gas prices may squeeze vehicle miles traveled, but those are anticipated to be transitory. Kent handed the session over to McKenzie to discuss patterns of data contributing to the “why” of changing rates.

McKenzie presented a cost-driver framework where we traditionally experience a lag from cost increases in claims to the appropriate rate action needed to return to profitability. The ratio-based framework relates premiums to fund expected losses (frequency × severity), expenses, and cost of capital. The consequence of this framework is that distributional effects matter. Any rise in costs on smaller incomes moves the ratio higher faster for those households.

McKenzie covered a litany of factors influencing frequency and severity. One slide on increases covered almost a dozen things, including inflation in used vehicle actual cash value, increases in repair costs, and a change in the mix of vehicles demanded by consumers shifting to SUVs, with many accumulating in an additive set of higher incidents, costs, and expenses. One unintended consequence for consumers is that some may resort to fraudulent behavior to reduce their own costs, ultimately shifting additional expenses onto the broader insured population.

McKenzie mentioned the ongoing concerns about how tariffs might exacerbate everything else going on and suggested some ways to stay aware of developments on both direct and indirect impacts. She noted we may be only at the beginning of the process to observe tariff-driven costs.

Smollik’s key focus was loss-reduction strategies. The big first move, he said, would be to not crash at all, followed by more driver awareness to mitigate when you can’t eliminate an accident. Advanced Driver Assistance Systems (ADAS) technologies and “put your phone down” campaigns enhanced with behavioral scoring and telematic adoption are making wide improvements. Better cost management of repairs and more efficiency in claims processing are also key strategies. But the overarching strategy is to align risk-based pricing to better match price to risk and reduce subsidies across consumers.

When it comes to systemic and jurisdictional opportunities to contain costs, Smolik pointed to some positive improvements in managing legal expenses and mitigating fraud. Specifically, he pointed to regulatory reforms, improving consumer education on risk and risk transfer funding (shopping for insurance), and some specific legislative reforms, notably in Florida and Michigan, where reforms are lowering insurance costs.

Finally, Smolik drew a line connecting the responsiveness of state departments of insurance to industry filings, which made the point that the slower a state moves on requests, the worse their constituent consumers experience adverse affordability as measured by the existing affordability index.

In the wrap-up and key takeaway summary and then an abbreviated Q&A session, it was noted that public policy concerns are part of actuarial considerations and recommendations. The group explained how dynamic the last five years have been in changing loss ratios for the industry and changing affordability ratios for consumers.

The impact of original equipment manufacturers overloading vehicles with features and driving new car costs to the highest rates on record was not lost on the audience. When the value at risk increases, costs for insurance usually do as well. It’s not all consumer preference driven, but where that is a factor, it is a sustained cost driver at the core of the process. A potential silver lining discussed was the growing adoption of accident-avoidance and safety technologies, which could eventually help reduce insurance costs; however, because turnover across the nation’s vehicle fleet occurs gradually, any broad risk-based rate reductions are likely to emerge slowly and only over time.