Contents

departments

- EDITOR’S NOTE

- Off the Radar

- President’s Message

- Articulating the Actuarial Value Proposition

- Member News

- Comings and Goings

- Calendar of Events

- In Remembrance

- In Memoriam

- CAS Staff Spotlight

- CAS Hosts the 2nd International General Insurance Teaching Summit in Bangkok

- New FCAS and ACAS Admitted or Recognized in May 2026

- Professional Insight

- Developing News

- Insuring Solar Storms: Modeling Considerations for Space Weather Risks in Insurance Contracts

- An Uncertain Policy: Tariffs and the Future of P&C Insurance

- Navigating Risk and Fairness in P&C Insurance with Algorithmic Auditing

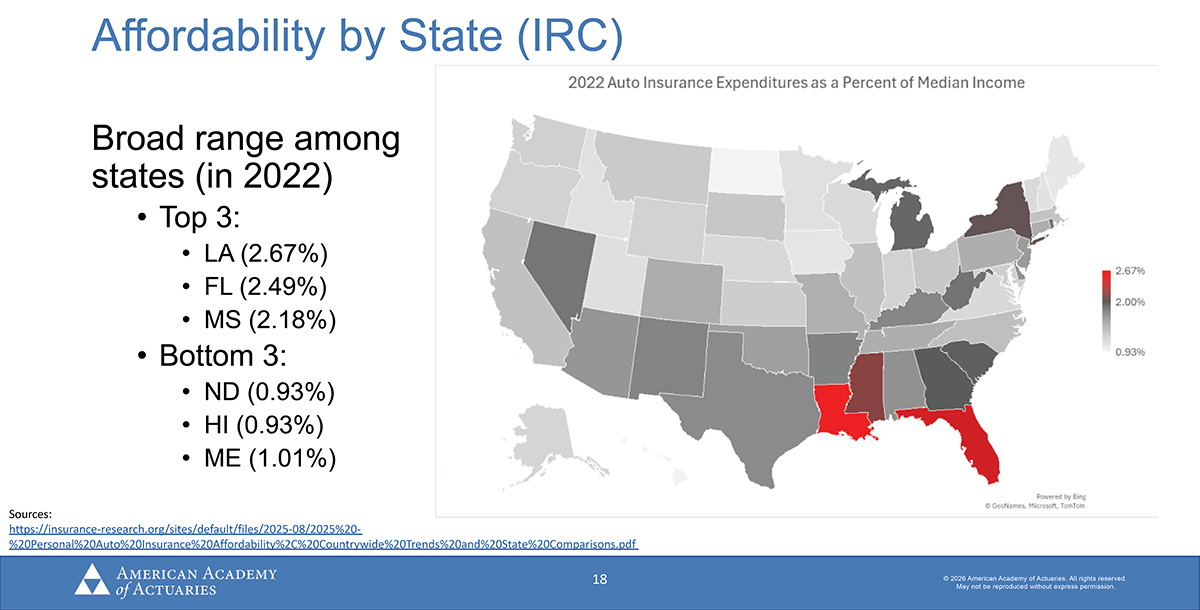

- Cost Drivers and Affordability in Personal Automobile Insurance

- Do You Have What It Takes to Be in the C-Suite?

- Actuarial Expertise

- An Actuarial Quartet

- Viewpoint

- Exams Reveal Much More than What You Know: Mosely Addresses New CAS Members at CAS Spring Meeting

- Minus Log Two — An Actuarial Poem

- Solve This

- It’s a Puzzlement

on the cover

-

An AI-fueled shock to insurance broker valuations offers a window into how technology could transform insurance markets and actuarial practice.

-

Who will help shape the future of the CAS? Meet the nominees for president-elect and the Board of Directors as they share their leadership priorities, perspectives on emerging challenges, and vision for the profession, ahead of this year’s election.

-

Explore key insights from the 2026 CAS Spring Meeting, from leadership and career growth to insurance affordability, algorithmic fairness, and the impact of tariffs on the P&C industry.

The amount of dues applied toward each subscription of Actuarial Review is $10. Subscriptions to nonmembers are $50 per year. Postmaster: Send address changes to Actuarial Review, 4350 North Fairfax Drive, Suite 250, Arlington, Virginia 22203.

Masthead

-

Editor in Chief

Jim Weiss

-

CAS Director of Publications and Research

Elizabeth A. Smith

-

AR Managing Editor and CAS Editorial/Production Manager

Sarah Sapp

-

CAS Managing Editor/Contributor

Greg Guthrie

-

CAS Graphic Designer

Sonja Uyenco

-

CAS Cross-Functional Coordinator/Contributor

Delilah Barrow

-

News Editor

Sara Chen

-

Opinions Editor

Richard B. Moncher

-

Editors

- Colleen Arbogast

- Daryl Atkinson

- Karen Ayres

- Glenn Balling

- Robert Blanco*

- Lisa Brown

- Michael Budzisz

- Sumanth Chebrolu

- Todd Dashoff

- Daniel Jay Falkson*

- Stephanie Groharing

- Julie Hagerstrand

- Srinand N. Hegde*

- Cameron Herrmann*

- Kenneth S. Hsu

- Cindy Hu*

- Jack Huang*

- Rachel Hunter*

- Rob Kahn*

- Benyamin Kosofsky

- Julie Lederer

- Albert Lee

- David Levy

- James Li*

- Sydney McIndoo

- Stuart Montgomery

- Sandra Maria Nawar*

- Erin Olson

- Shama S. Sabade

- Michael Schenk

- Robert Share

- Craig Sloss

- Jared Smollik

- Andrew Somers*

- Bella Thiel*

- Isaac Wash*

- Radost Wenman

- Ian Winograd

- Vanessa Wu*

- Xuan You*

- Yuhan Zhao*

-

*Writing Staff

-

Puzzle

Jon Evans

-

Advertising

Al Rickard, 703-402-9713

arickard@assocvision.com -

The Casualty Actuarial Society is not responsible for statements or opinions expressed in the articles, discussions or letters printed in Actuarial Review. -

For permission to reprint material from Actuarial Review, please write to the editor in chief. Letters to the editor can be sent to AR@casact.org or the CAS Office. To opt out of the print subscription, send a request to AR@casact.org.

Images: Getty Images -

© 2026 Casualty Actuarial Society.

ar.casact.org

Off the Radar

n old expression goes that markets hate uncertainty. Stock prices often plummet before presidential elections, during geopolitical conflicts, or after unexpected news ranging from earnings shortfalls to global pandemics. An inversion of the adage goes that markets love uncertainty because perceived risk gives investors opportunities to demand steep discounts. The S&P 500’s recent price-to-earnings ratios suggest markets feel rather certain that the AI-powered future will be lucrative.

Ironically, Wall Street’s confidence resembles the self-assurance radiating from AI tools such as Claude or Gemini. Since inception, these large language models have been maligned for their sycophancy and tendency to hallucinate. But publicly traded insurance brokers may have thought they were the ones hallucinating when they collectively shed billions in market capitalization earlier in the year. John Divine unpacks the AI-driven uncertainty in his cover story, “Stock Shock.”

In this environment, former CAS president Roosevelt Mosely’s address to new members from the CAS Spring Meeting — which we feature in this issue of AR — particularly resonates. “The hardest questions are rarely about calculation,” he told attendees. “They are about judgment, weighing tradeoffs, and explaining uncertainty honestly rather than hiding it.” Two quartets in this issue of AR aspire toward such a mindset. Developing News provides its trademark measured discussion of four hot topics, while Dave Clark’s actuarial quartet visualizations prove truth is rarely limited to what the eyes see.

The truest disruptions fly furthest under our radars. Readers may be monitoring hantavirus or Ebola outbreaks a world away, but Zoë FS Rico’s and Yanisa Cheeppensuk’s solar storm coverage illustrates how significant risks to our interconnected world emanate from the sun. With uncertainty being the greatest certainty, actuaries’ best recourse is neither love nor hate, but rather, accept. In Mosley’s words, “Being comfortable with ambiguity doesn’t mean being unsure. It means being thoughtful. It means knowing what you know, acknowledging what you don’t, and still being willing to act.”

Actuarial Review

Casualty Actuarial Society

4350 North Fairfax Drive, Suite 250

Arlington, Virginia 22203 USA

Or email us at AR@casact.org

Articulating the Actuarial Value Proposition

ne of the most enjoyable experiences during my year as president-elect, and thus far in my presidential term, has been the opportunity to visit with employers of CAS members. A typical employer visit consists of a town hall with the entire actuarial department and a separate smaller meeting with the actuarial leadership team. The town hall includes a CAS update presentation, followed by a usually lively Q&A session, while the actuarial leadership meeting focuses on topics of concern to management, industry trends, and the CAS/employer relationship. These conversations provide valuable opportunities for us to hear what the CAS is doing well, how we can improve, and how we may be able to provide additional value to the employer community.

In one conversation with the actuarial leadership team of a large employer of CAS members, the chief actuary shared that he was challenged during every budget cycle on the number of actuaries on staff, the cost of exams, membership dues, attendance at educational conferences, etc., and noted it would be helpful if the CAS had anything in the way of data or supporting materials that would demonstrate the value of employing actuaries. This resonated with me because I was similarly challenged by my CFO during my tenure as chief actuary (and previously as chief risk officer, though not specific to actuaries in that case). In subsequent employer visits, I posed this question to actuarial leaders, and they nearly all agreed this was an ongoing challenge for them. I’ve given this some thought (and consulted a couple of AI tools) and believe the actuarial value proposition is quite strong and can be viewed across five dimensions.

#1. Decision-making under uncertainty

- Better pricing and profitability decisions.

- More accurate forecasts.

- Stronger capital allocation.

- Fewer surprises.

In short, actuaries give executives the confidence to act decisively when the future is anything but certain.

#2. Financial stability

- Maintain adequate reserves.

- Optimize capital requirements.

- Reduce earnings volatility.

- Strengthen balance sheet resilience.

In short, actuaries safeguard the organization’s financial backbone.

#3. High integrity expertise

- Advice they can trust.

- Independent, objective analysis.

- Decisions backed by a globally recognized profession.

That credibility carries weight with regulators, auditors, boards, and rating agencies.

#4. Insight across the enterprise

- Mergers and acquisitions due diligence.

- Product strategy.

- Risk appetite and governance.

- Investment and asset liability management.

- Scenario planning and stress testing.

They help leadership teams see around corners and act before others do.

#5. Competitive advantage through better risk intelligence

- Predictive modeling.

- Behavioral insights.

- Market and demographic trend analysis.

- Early warning indicators.

This enables executives to act proactively rather than to react defensively.

Taken together, these five dimensions make a compelling case. Actuaries do far more than support technical insurance functions; they strengthen decision quality, financial resilience, and strategic execution across the enterprise. That reality reflects the breadth and depth of the CAS syllabus, the relevance of continuing education, and the preparedness of CAS members to solve complex business problems well beyond pricing, reserving, and capital modeling. In fact, I can think of no other profession or discipline with a comparable degree of versatility. That is why it is important for actuarial leaders to clearly articulate the actuarial value proposition and to defend related staffing levels and expense budgets.

Staff functions are generally under greater budget pressure than customer-facing and market-facing teams. Because actuaries are well compensated, it is not surprising that their staffing and expenses come under scrutiny from time to time. That said, actuarial compensation is market driven and represents an objective measure of the value actuaries bring to an organization. The real issue, then, may be less about how many actuaries an organization employs and more about how they are being used. If actuarial departments do not keep evolving by adopting new technologies, improving efficiency, and shifting capacity to visible, value-added work, CFOs will reasonably expect the required number of actuaries to level off or decline over time.

Actuaries have become indispensable in the traditional insurance functions of pricing, reserving, and capital modeling, so the challenge and opportunity is to make ourselves equally indispensable in other critical areas — strategic planning, claims, underwriting, product development, compliance, risk management, operations, business development, and more. There are many examples of actuaries providing significant value in these areas, but unfortunately, actuaries in these areas are the exception and not the norm. In my experience, once a nonactuarial function has had the benefit of having an actuary on their team, they are loath to give up that capability, so perhaps the opportunity lies in getting more actuaries engaged in nontraditional business areas.

What is an actuarial leader to do when challenged on staffing levels and expense budgets, particularly in the face of AI and rising expectations for gains in both efficiency and analytical capability? My first observation is that once the question has been asked and expense reduction targets have been set, it is often too late to avoid the challenge. The better approach is to be proactive by taking a long-term view of staffing and expenses and acting deliberately to demonstrate the actuarial value proposition.

One essential part of that approach is consistently communicating the work actuaries are doing and the value they are creating across these dimensions, while highlighting and recognizing significant contributions whenever possible. Wins in market-facing and customer-facing business units are rightly celebrated, but the enabling achievements of staff functions often receive far less visibility. Creating opportunities for recognition of actuarial accomplishments achieves two important things: It strengthens engagement within the actuarial team, and it reinforces to leadership the distinctive value actuaries bring to the enterprise.

Equally important is the need to challenge yourself and your team to drive as much efficiency as possible within the actuarial function and to make whatever organizational changes are needed to reflect those gains. This may, and likely should, lead to reduced staffing in some areas. But the key is to have already identified where that capacity can be redeployed to higher-value work that is visible, strategically important, and worthy of recognition.

Actuarial Review Letters Policy

Letters shall not contain personal attacks or statements directly or implicitly denigrating the characters of individuals or particular groups; false or unsubstantiated claims; or political rhetoric. Letters should be no more than 250 words and must include the author’s name and phone number or email address, so the editorial staff can confirm the author. Anonymous letters will not be published. There shall be no recurrence of topics; issues previously addressed will not be the subject of continued letters to the editor, unless new and pertinent information is provided. No more than one letter from an individual can appear in every other issue. Letters should address content covered in AR. Content regarding the CAS Board of Directors or individual departmental policies should be directed to the appropriate staff and volunteer groups (e.g., board, working groups, committees, task forces, or councils) instead of AR. No letter that attempts to use AR as a platform for an ulterior purpose will be published. Letters are subject to space limitations and are not guaranteed to be published. The AR editorial volunteer and staff team reserves the right to edit any submitted letter so that it conforms to this policy. Decisions to publish letters and make changes to submissions shall be made at the discretion of the AR Working Group and CAS staff.

For more information on AR editorial policies, visit here.

Another powerful tool is sharing the wealth. Look for opportunities to place actuaries in other business functions where they can add value, even if they remain on the actuarial function payroll for a period. This facilitates the expansion of actuarial influence, generates business and organizational insights for the actuarial function, provides invaluable cross-training opportunities, and further demonstrates the value of actuarial capabilities across the organization.

Finally, a long-term view of staffing and expenses also requires recognizing that there will be times when a temporary step backward is necessary to enable future progress, especially when an organization is under meaningful budget pressure and every function is affected. In those moments, acting as part of the broader enterprise and sharing in the financial discipline of the organization can be just as important as protecting your own budget and team in the short term. Maintain the long-term focus, continue looking for ways the actuarial function can add value, and when the time comes to invest in talent again, actuaries should be at the top of the list.

The next time actuarial leaders want to know how the CAS can help them in articulating the actuarial value proposition, I will have a better answer for them!

Comings and Goings

Salmaan K. Allibhai, FCAS, has been promoted to executive vice president, chief analytics and technology officer at Kinsale Capital, expanding his role to oversee both data analytics and technology functions. Allibhai joined Kinsale Capital in April 2016 and previously served as senior vice president and chief actuary.

Erika Schurr, FCAS, FCIA, has been appointed senior vice president and chief actuary at Definity. With more than 20 years of P&C insurance experience, Schurr previously served as chief actuary at Travelers Canada and joined Definity as part of its recent acquisition of Travelers Canada. Her volunteer roles on many industry committees, including the Canadian Institute of Actuaries’ P&C Financial Reporting Committee, the Property and Casualty Insurance Compensation Corporation’s Actuarial Advisory Committee, and the Insurance Bureau of Canada’s Nat Cat and Climate Standing Committee, reflect the depth of expertise she brings.

Calendar of Events

-

September 14–16, 2026

2026 Casualty Loss Reserve Seminar

Las Vegas, NV -

November 8–11, 2026

2026 CAS Annual Meeting

Honolulu, HI -

December 3, 2026

2026 CAS Canada Connection

Montreal, Quebec, Canada

In Remembrance

The Volunteer and Sportsman

1942–2026

Arthur Robert Cadorine passed away in April 2026. Cadorine was born in Brooklyn, New York, to Arthur F. Cadorine and Catherine Cadorine (Weber). Cadorine was a lifelong New Yorker. He graduated from St. John’s University with a B.S. in mathematics and married the love of his life, Linda M. Cadorine (Rodriques), on July 9, 1966. Cadorine had a long and distinguished career as an actuary with the Insurance Services Office (later known as Verisk Analytics) and was a proud member of the CAS. Though he volunteered for multiple CAS committees, he was most remembered for his work on the Ratemaking Seminar Committee, known as the Ratemaking, Product, and Modeling Seminar Working Group today. Cadorine was an avid golfer and devoted New York Yankees and New York Jets fan and played tennis for many years. He is survived by his wife, Linda Marie Cadorine; daughter Jessica Cadorine; his grandchildren, Andrew and Caroline Caruso; and his nephew Robert Cadorine.

The Humble Traveler

1962–2026

Tom Allen Smolen passed away in Norwalk, Iowa, in May 2026. He was a dearly beloved husband to Patty Smolen; father to Matthew Smolen, Brendan (Alyssa) Smolen, and Corrine (Will) Searight; grandfather to Caleb, Olivia, and Noah Smolen; brother to Jan (Gary) Lieberman; and uncle to many nieces and nephews. Smolen was born on May 1, 1962, to Darlene and Al Smolen in Santa Rosa, California, where he was raised. He graduated from the University of California, Berkeley, in 1984. He met Patty, his wife of 38 years, while they were working as actuaries at Fireman’s Fund Insurance in Novato, California. Job changes brought Tom to Des Moines in 2004, where he advanced to a senior position at Nationwide Insurance. After a 30-year career as an actuary, he took an early retirement in 2014. In retirement, he enjoyed golf, traveling with Patty, and playing cribbage and poker with friends. His true vocation in retirement was volunteering. He spent many years with Mercy Hospital in Des Moines, with St. John the Apostle Catholic Church as an organizer for Connection Café meals, with the Habitat for Humanity Core Crew salvaging materials for Habitat’s ReStore, and with the Knights of Columbus at St. John’s. Smolen was a humble man, never looking for recognition of his service, but helping those he could.

In Memoriam

1939–2026

Arthur R. Cadorine (ACAS 1969)

1942–2026

Cynthia M. Potts (FCAS 1982)

1955–2005

Tom Smolen (FCAS 1990)

1962–2026

CAS Staff Spotlight

Meet Delilah Barrow, Cross Functional Program Coordinator

Delilah Barrow

elcome to the CAS Staff Spotlight, a column featuring members of the CAS staff. For this spotlight, we are proud to introduce you to Delilah Barrow.

- What do you do at the CAS? How does your role support the Strategic Plan?

As a program coordinator at the CAS, I support multiple departments, including Professional Education, Meeting Services, and Publications and Research. My role involves coordinating in-person, virtual, and hybrid events, managing livestreams and learning platforms, supporting research grant processes, maintaining program websites, coordinating vendors, and preparing reports and communications for members and stakeholders.Because my role touches many areas of the organization, I help ensure that programs, educational offerings, publications, and events are delivered efficiently and with a high level of quality. By improving coordination, supporting member engagement, and helping teams make data-informed decisions, I contribute to CAS’s goal of providing exceptional professional development and resources to its members.

- What inspires you in your job? What do you most love about your job?

What inspires me most is knowing that my work helps create meaningful learning opportunities and professional experiences for CAS members. Whether I’m helping coordinate a major educational event, supporting research initiatives, or improving processes behind the scenes, I enjoy being part of work that helps professionals grow and advance in their careers.What I love most about my role is its variety. Every day is different, and I have the opportunity to collaborate with multiple departments, learn new technologies, solve problems, and contribute to projects from planning through execution.

- Describe your educational and professional background. What do you bring to the organization?

My professional background spans more than 10 years in program management, nonprofit operations, and organizational development. I’ve managed large-scale programs, overseen grants and contracts, implemented technology solutions, and developed systems that help organizations operate more effectively.One of the most rewarding experiences in my career was leading a digital inclusion program that served more than 2,000 older adults across Washington, D.C., helping them build confidence using technology and access important online resources.

At the CAS, I bring strong organizational and project management skills, a collaborative mindset, and a passion for continuous improvement. I enjoy solving problems, creating efficient processes, and helping teams succeed. Most importantly, I strive to lead through service and support others in achieving their goals.

- What is your favorite hobby outside of work?

Outside of work, I enjoy gardening and homesteading on my property in Southern Maryland. I’m currently building vegetable gardens, planting fruit trees, and learning more about sustainable living. I love seeing something grow from a simple idea into something that can nourish and bring people together. - If you could visit any place in the world, where would you go and why?

I would love to visit Kenya. I’m fascinated by its natural beauty, wildlife, and cultural diversity. Experiencing a safari, learning about local traditions, and seeing the country’s landscapes firsthand would be an unforgettable experience and an opportunity to gain a broader perspective on the world. - What would your colleagues find surprising about you?

Many of my colleagues would be surprised to learn that I enjoy making natural skincare products and have a passion for cooking and catering. I love creating things from scratch, whether it’s a skincare recipe, a meal for family and friends, or a special event. Both hobbies allow me to express my creativity and bring people together. - How would your friends and family describe you?

My friends and family would describe me as dependable, resourceful, and caring. They know that when challenges arise, I’m usually focused on finding solutions and helping others navigate obstacles. They would also describe me as a servant leader — someone who genuinely enjoys helping people grow, succeed, and reach their goals. Whether I’m supporting my family, mentoring someone professionally, or volunteering in my community, I find fulfillment in helping others and making a positive impact.

CAS Hosts the 2nd International General Insurance Teaching Summit in Bangkok

he CAS recently hosted its second International General Insurance (GI) Teaching Summit, held May 21–22, 2026, in Bangkok, Thailand. The event brought together actuarial science educators from across Asia to advance the future of GI education. More than 40 universities were represented, a notable increase from the attendance at the 2024 summit, indicating a growing interest in building academic programs that prepare students for careers in GI.

Bottom: Sathya Sai Mudigonda gives a demonstration of a case study focused on extended warranties.

The summit featured presentations from some of the winners of the 2025 CAS Case Study Creation Challenge, highlighting a diverse array of innovative approaches to topics such as sustain ability risk management, catastrophe modeling, insurance fraud detection, and extended warranty protection. Additional sessions focused on actuarial leadership in climate resilience, integrating communication and professional judgment into the curriculum, and preparing students for an AI-enabled profession.

Each session throughout the summit featured faculty participation. This created a space for meaningful dialogue and collaboration on opportunities and challenges in GI education for educators throughout the region. Artipania, a Thailand-based visual facilitation group, brought the summit’s insightful conversations to life through bold and engaging graphic reporting.

CAS President Barry Franklin opened the summit with remarks emphasizing the evolving role of actuarial education and the importance of equipping students with both technical expertise and professional skills for success in the modern workplace.

“As educators and industry leaders, we all share a common interest in preparing students not only to succeed on actuarial exams, but also to become thoughtful, technically skilled, and globally minded professionals who can help organizations navigate an increasingly complex risk environment,” Franklin remarked.

As the summit concluded, participants left with new professional connections, fresh perspectives, and a shared commitment to strengthening the future of general insurance education across Asia and the global actuarial community.

New Fellows Admitted or recognized in May 2026

Row 2, left to right: Ken Zesso-Hoernis, Shannon Cikowski, Emily Saint Marie, Benjamin Thomas Pennings, Vadim Semenikhine, Yiming Yuan, Matthew Cain, Shannon Osterfeld.

Row 3, left to right: Andrew P. Heyse, Andre Douglas Aubert, Joseph Fafian, Eric Amstislavskiy, Daniel Harris, John Donato, Christopher Loren Lubow.

Row 2, left to right: Myron Yang, Ruiqi Liang, Fan Feng, Shariq Sadiq, Robert Daniel Moser, Shuangjia You.

Row 3, left to right: Spencer Balonis, Gage Haby, Jabari R. Washington, Clinton McCullough, Mason C. Spitz, Colin Bailey, Sean Thomas Costello.

Row 2, left to right: Andrew Craig, Huaming Yan, John James Mcnulty, McKay Gerratt, Jean-Philippe Quirion, Ankit Singh Anand.

Row 3, left to right: Constantine W. Chan, Victor (Weitao) You, Josh Herrera, Brandon Florizone, Alexandre Gagnon, Ryan Dowdle, Tanner Downs.

New Associates Admitted Or Recognized In May 2026

Row 2, left to right: Diana Manuela Dodu, Luke S. Stees, Zachary Boc-Jyh Grasty, Jarod Wallen, Faisal A. Alabsy, Dylan Baliesh, Samuel Forest, Laurie-Eve Bastiani.

Row 3, left to right: Bohong Qian, Lucas Fernandez-Fraga, Megan McFarland, Eric Rolfes, Jacob Daniel Savage, Scott Harrison Shanbom, Sean Kinsman.

Row 2, left to right: Maya Digirolamo, Eva Mary Shanker, Richard Li, Alec Warden, Quincy Clare-King, Nicholas Adam Cottrell, Nicholas Camacho, Caleb Dahlstrom.

Row 3, left to right: Hayden Thomas Lieb, Matthew David Unrau, Dmitriy Tigunov, Jacob Walsh, Thomas Allen Fuller, Connor Glinski, Si Miao.

Row 2, left to right: Tyler James Clearwater, Micah Eigbrett, Michael John Thomson, Emma Schwartz, Elisha Wilson, Christine Landry, Rebekah Casino, Carter Khoury, Julia Lynn Rothstein.

Row 3, left to right: James Martin Milleville, Grant Jones, Riley Ross Phillips, Serjan Bratic, Zack Snider, Jason J. Rutten, Christopher Lepore, Seth Mckinney.

Row 2, left to right: Michael Canlas, Joseph L. Jackson, Yuyang Chen, Benjamin Codey Cotton, Daniel South, Winson Lei, William Oherron, Joseph David Perreault.

Row 3, left to right: Nicholas Kellington, Trevor Parish, Gordon Li, Adoniadis Savidis, Beryl Daniel Munson, Hantao Wang, John E. Keenan, Shuo Zhang.

Row 2, left to right: Christopher James Shields, Gagan Umesha, Srikar Emandi Sunil, Zheng Xun Hong (Kyle), Amber Jensen Mickelson, Kinsey Miller, Mariane Da Sylva.

Row 3, left to right: Brayden Edgar Walcarius, Conrad Jureczek, Lucas Joseph Scanna, Luca Rzewski, Bennett Stefanowicz, Jerry He, Wyler Lukas Lubeck.

Row 2, left to right: Sarah J. Johnson, Christophe Veillette-Cloutier, Bartholomew Ghanney, Nathan Olander, Mufaro Chitakure, Surbhi Gupta, Yu Wei Huang, Gabriel Cobzaru, Peter Park.

Row 3, left to right: Won Suk Ji, Nathan Hastreiter, Samuel Joseph Schaefer, Alec Karal, David Dexter, Spyros Orfanos, Nathan Kan, Patrick DiRoma, Bo Lin.

Row 2, left to right: Kimberly Paige Sheehan, Franklin Scott Ferrell, Sy Bonneau Neeley, David Schumann, Robert Hinrichsen, Alexander Del Valle Leather, Chelsea Hidden.

2026 CAS Election

AS voting members (all Fellows, plus Associates who have been members for at least five years) will have the opportunity to vote on a slate of candidates for the CAS Board of Directors and CAS president-elect, with online voting beginning on June 30, 2026. On that day, voting members will receive an email with a link to the online ballot. Completed ballots must be submitted online by July 28, 2026.

Below, each candidate has provided a 100-word summary regarding their interest in running for CAS leadership positions. Additionally, to give voters a clearer, easier way to compare candidates’ thinking on important CAS priorities, candidates answered a shared set of questions built around the strategic issues members said they most wanted addressed. More details about each candidate can be found in the Meet the Candidates section of the CAS website.

Please contact Mike Boa with any questions or comments about the election process.

My candidacy reflects a commitment to steady, thoughtful, and globally informed leadership. An international career across North America, Europe, and emerging markets has given me a broad perspective on how actuarial work is applied in different contexts. Experience across both established and developing markets informs my approach to actuarial practice, governance, and professional stewardship. I value the universality of actuarial principles and the importance of applying them with sound judgment and context. This perspective underpins a pragmatic leadership style focused on strengthening member value, supporting high standards, and ensuring the CAS remains relevant and engaged across geographies, markets, and career stages.

The actuarial profession has successfully adapted to technological change many times. I believe that AI, machine learning, and agentic systems present the most transformational shift since mechanical computation. We must evolve our education and public perception, so we remain relevant and continue our core purpose: understanding, educating, and managing financial risk. Serving on the Nominating Committee and as VP, Research and Practice Advancement, I have seen the passion our leaders bring to serving the CAS. I am running because I am deeply grateful for the opportunities I have received, and I want this path for professional fulfillment to stay open for future actuaries.

I am running for the CAS Board to strengthen the CAS’s member value and global relevance. I bring international property/casualty experience and a practical board perspective from leadership roles in consulting, as a chief risk officer, and current positions as independent non-executive director across multiple London Market and Lloyd’s insurers. I previously served as VP, International, delivering a new cost-effective international strategy that expanded CAS engagement, membership, and influence globally. Since my prior Board term over 10 years ago, the CAS has evolved significantly; I am eager to return to the Board and help navigate these changes with a collaborative, member-focused approach.

AI’s rise makes a strong actuarial profession more essential than ever. Our discipline is distinctive in its understanding of both the power and limits of data, as well as in harnessing algorithms in ways aligned with regulation and societal values. This gives us tremendous potential to help society adapt to AI and to ensure that future iterations of AI are well adapted to the needs of business and society. I focused my career on deepening our profession’s foundations and expanding its footprint in the data science era. I would like to help the CAS continue this work in the AI era.

I am running for the CAS Board to advocate for our profession and the actuaries who shape it. Over my 20-year career, our profession has navigated several inflection points, as data and technology have changed how we understand and manage risk. We are again at such a moment, with advanced analytics and AI accelerating that change. In this environment, the CAS plays an essential role in ensuring actuaries remain trusted and influential experts in risk and insurance. I want to build on our existing strategy so the CAS continues to honor its legacy while developing agile, forward-looking actuaries who can grow, adapt, and lead.

I have been a volunteer with the CAS ever since I received my credentials over 20 years ago. Giving back to the profession is important to me, and I would bring my experience and passion to the CAS Board of Directors. Through my committee involvement, I have been working on innovative ways to provide educational opportunities to all members, whether they are new in their career up to the C-suite. Through the CAS Board, I would like to continue to look for these opportunities and continue to broaden our outreach to aspiring CAS members.

My candidacy reflects a commitment to shaping a resilient, forward-thinking actuarial profession. I am passionate about supporting members at every stage of their career, from advocating for candidates throughout the exam program to empowering credentialed actuaries to lead in emerging spaces. My professional experience across leadership and practitioner roles, combined with my personal perspective as a mom, shapes how I lead: with authenticity, creativity, practical problem-solving, and care for future generations. As AI advances, the CAS is uniquely positioned to champion ethical use, rigorous validation, and education opportunities to uphold the excellence of our credential for current and future actuaries.

I was graduating with a math degree and no clear direction. My mom joked I’d end up working at Burger King. Then a professor said, “There’s this actuary thing — you should look into it.” That “actuary thing” gave me a career I love, lifelong friends who have shaped my path, and a profession worth fighting for. Now I want to give back to the CAS with the same intensity and purpose it gave me. Serving on the Board is a chance to pay it forward, drive meaningful progress, and help the CAS adapt, evolve, and lead with confidence.

With 25 years of CAS membership and extensive volunteer leadership, I am committed to advancing the CAS’s independence and relevance and the future-ready skills of its members. My priorities include enhancing the candidate experience by more proactively adding cutting-edge material to and removing outdated content from the syllabus and ensuring robust exam-day technology safeguards. I will also champion initiatives to prepare members for rapid change, including leadership and business skills, and responsible adoption of AI to better serve their employers and clients. I am eager to contribute my experience, energy, and dedication to help the CAS evolve and thrive sustainably.

STOCK SHOCK

the AI in Volatility

STOCK SHOCK

t a glance, February 9, 2026, was a rather rosy Monday on Wall Street: The S&P 500 added 0.5%, the Nasdaq jumped 0.9%, and the Dow Jones Industrial Average eked out a modest gain but nonetheless closed at a new all-time high.

But for the insurance sector — and brokers in particular — February 9 was a day of reckoning.

The S&P 500 Insurance Index (^SP500-4030) took a 3.9% haircut.1 The MarshBerry Broker Composite Index cratered 8.9%.2 Brown & Brown (–6.9%), Marsh McLennan (–7.5%), Ryan Specialty (–7.9%), Aon (–9.9%), Gallagher (–9.3%), and WTW (–12.1%) all gave up billions in value. It was WTW’s worst one-day loss since November 2008.

Behind it all was a double whammy of bad-sounding news from the world’s favorite AI chatbot, ChatGPT.

First, a company called Insurify launched what was heralded as the first insurance comparison app within ChatGPT, allowing users to compare car insurance rates via natural conversation. Any actual purchases would be made on Insurify’s own website.

The second bit of news was even more alarming for investors. Tuio, a Spanish insurer, became the first company approved by OpenAI to offer personalized home insurance quotes within ChatGPT.

“For the first time, an insurance provider can distribute its products and offer quotes directly inside an AI platform where hundreds of millions of insurance buyers are already performing their research,” OpenAI boasted in a statement.3

While neither application allowed users to directly buy policies within ChatGPT, and Tuio’s integration is not available for U.S. users, the headlines created fear, and markets ran with it.

For Meyer Shields, managing director and equity research analyst at Keefe, Bruyette & Woods, this extrapolation seemed a bit dramatic.

“This is not the first time that we’ve seen some sort of ’apocalyptic’ scenario for the insurance brokers. I’ve been in the industry a little more than 30 years, and it comes up a lot,” Shields says, saying it’s the same argument that was made at the dawn of the internet.

The result? Three decades on, there’s been some success with direct-to-consumer car insurance online, but there are still basically just three main players in that market: Progressive, GEICO, and Allstate.

“Fundamentally it does not look like people want to buy even the very simple products using technology as opposed to an agent … I look at homeowners penetration in direct-to-consumer. It’s probably less than 10% — maybe 7% or 8%. And next to auto, that’s probably the second-most homogeneous insurance product,” Shields says.

So if the AI drama is overblown, why has the impact on market prices endured?

As of the closing bell on April 17, all six broker stocks mentioned above still traded below their closing price on February 6 (the last trading day before GPTgate), despite the S&P 500 adding a healthy 2.8% over the same period.

What gives? Does this industry have a new risk profile due to a secular change in the way of doing business, or is this just another example of Wall Street myopia?

The bear case: Where AI actually threatens brokers

“I do think it’s going to affect top-of-the-funnel kinds of markets more than commercialized markets. So think personal lines, homeowners, and personal auto — more than complex advisory risks and things like that,” says Farah Ismail, head of commercial lines for ICT (Insurance Consulting and Technology) at WTW.

Brokers profit from information asymmetry, and AI levels that uneven playing field for simple products. If you’re factoring in AI as a major new force threatening to change business as usual, look for personal lines to be tested at the vanguard.

Conversely, “specialty, commercial, and multi-line risks need bespoke coverage. There’s more underwriter judgment, there’s more negotiated terms … and from a broker revenue standpoint, the bulk of that revenue sits on the commercial, specialty, multi-line side,” Ismail says.

Tracy Dolin-Benguigui, director and senior research analyst covering life and non-life insurance at Wolfe Research, hammers this point home with an example.

At a Gallagher (AJG) investor day in March, AJG “basically said they had identified $500 million of premiums that they place that are either personal lines or micro-commercial, and then they took a deep dive and really only identified $200 million of those premiums as more susceptible to AI risk,” Dolin-Benguigui says.

“That represents something like 1% of their global revenue” after accounting for commissions, Dolin-Benguigui notes. “So it’s pretty contained.”

Raphaël Vullierme, co-founder of WaniWani, the AI distribution infrastructure that powered the Tuio/ChatGPT insurance app integration, agrees that the risks to brokers are contained — for now.

In the short-term, he admits that complex and commercial risks are essentially safe from disruption. Risk managers want to go through real people, and more commoditized personal lines make for easier pickings.

Look beyond the next few years, however, and Vullierme — who himself co-founded Luko, which grew to become France’s largest online home insurer — thinks things could change quickly.

“There’s nothing really complex in matching risk capacity and demand that AI in 10 years won’t be able to do,” Vullierme says.

The internet helped commoditize the sale of goods, Vullierme says, but two frictions heavily insulated insurance brokers: buyers needing to provide complex personal inputs, and the difficulty of comparing bespoke products.

He sees AI dissolving both.

Introduced in November 2024, MCP was developed by Anthropic, the firm behind the Claude AI chatbot.

“It’s your AI as a buyer that’s going to speak to the AI of the seller and say, ’This is a business doing $10 million revenue, specializing in distributing pet food in Iowa.’” The technology now exists for your AI agent to communicate with the AI agent of an insurer to derive a customized commercial quote for your approval.

“This is going to create a lot of disruption in the market because two AIs can work together to build a custom offer. This was completely impossible two years ago without a human in the middle working for both sides. Now it’s possible for every kind of risk and every kind of business line,” Vullierme says.

While the technology might be ready, the U.S. regulatory landscape is not — and that’s a meaningful speed bump for AI-driven insurance distribution.

Spain’s Tuio operates under the luxury of a single European regulatory framework, while insurers in the U.S. navigate varying regulatory environments governing how policies can be marketed, quoted, and sold.

One example: Colorado’s SB 21-169,4 signed into law in 2021 and among the first AI-specific insurance regulations in the country, requires insurers to demonstrate that their AI-driven systems don’t unfairly discriminate against consumers. The law places the compliance burden squarely on carriers and any technology partners they use — meaning an AI app offering quotes inside ChatGPT would need to clear a higher bar in Colorado than in most other states.

Nationally, the NAIC’s Big Data and Artificial Intelligence Working Group5 is developing model frameworks, but adoption across states has been uneven, creating a regulatory patchwork that slows any national rollout.

None of this means AI-driven distribution won’t arrive in the U.S. But it does suggest that the timeline for the kind of seamless, in-app insurance purchasing that panicked investors on February 9 is longer — perhaps significantly longer — than the market’s one-day reaction implied.

The bull case: Why brokers (and actuaries) may benefit

“In reality, the app suggestion part from OpenAI is not working very well at the moment,” Vullierme said in a March 23 interview.

The idealized user flow has ChatGPT suggesting the relevant app for the user to utilize within the ChatGPT environment.

“But for now, the suggestion part of the app is not working very well, so the user needs to install or say ’@’ the name of the app to use it.”

Not only is the industry-killing AI chatbot integration not the frictionless disruptor people feared, there are also plenty of ways that AI is being deployed today that stand to benefit both brokers and carriers.

Shields says that both brokers and underwriters have expenses that should decline over time due to efficiencies brought on by AI and tech-enabled efficiencies. That’s a win-win-win for brokers, carriers, and consumers in theory, because in a competitive industry some of those lower costs will be evidenced in the lowered premiums.

Shields gives a simple example of how AI can shave costs for brokers: “If somebody submits an application and they’ve written in the address field using words like twenty-six instead of the number 2 6, that can take some time to digest, and we’ll soon, if we’re not already there, get to the point where that’s very easy to digest. That sort of small inconvenience adds up to a real cost to brokers that will go away.”

In a fragmented marketplace, Shields thinks brokers who invest in technologies that reduce the time to get customers a quote will see benefits accrue.

“The same way Progressive and GEICO have lowered overall industry costs because they’ve become bigger and their costs are lower, I think the big brokers will have that benefit as well,” Shields says.

For carriers, “the time between getting a submission from their broker and then being able to turn around an actual quote — that time has reduced quite substantially,” Ismail says.

Ismail also sees retention rates benefiting from automation “because you already did your due diligence the first time around. So you might be able to create much more robust guidelines on renewal to say, ’Look, as long as your exposure hasn’t changed dramatically, this is where we are on pricing.’”

Thus far, the ChatGPT disintermediation story is only a story. And while stories play an important role in short-term Wall Street gyrations, the early days of the ChatGPT-insurance app experiment have been anything but a slam dunk.

Shields, who strongly believes the February sell-off was overdone, succinctly sums up how he thinks about the “AI will kneecap brokers” narrative: “I think the upside to the brokers from making this a faster process far exceeds the few people likely to buy insurance without an agent.”

The actuarial angle: What changes in the models

Shields thinks so, but with a caveat. “It will impact retention, but I do think it’ll be gradual. All of these things manifest themselves much more slowly than modeling them on a spreadsheet might anticipate.”

And Ismail, while she’s seen an increase in retention in the short term, acknowledges it’s a double-edged sword if AI, for example, makes the submission ingestion process so seamless that buyers can “send [their] account to 12 different brokers at every renewal cycle and potentially make changes to [their] actual policy.”

For Vullierme, who has the benefit of seeing the cutting-edge AI use cases before the general public even knows they exist, there’s one nascent practice that could challenge traditional rules of thumb around quote-to-bind ratios.

“We have seen businesses implement procurement [AI] agents, so at the renewal date, there’s automatically a procurement agent that browses for new quotes without the business having to do anything,” Vullierme says.

He says AI agents may already be ringing call centers undetected, creating a higher volume of quotes, and dinging the quote-to-bind ratio or increasing churn.

But the changes aren’t all bad for industry mainstays, Vullierme says.

In commercial lines, he’s seeing people use ChatGPT or Copilot connected to their work environments. This means these programs are plugged into all sorts of other software — document management services, accounting software, payroll programs, contract management services — the whole kit and caboodle.

This allows businesses to answer quote questions far more easily because “AI is prefilling all the answers on behalf of users and the user just has to validate,” Vullierme says.

The ease of use allows insurers to ask new, more granular underwriting questions, creating new variables and new opportunities for pricing and underwriting, he says. “We think this will increase even further the power and importance of the pricing team.”

Of course, the degree to which organizations are embedding AI tools within day-to-day operations also presents new, potentially very large, risks that come with overreliance on any one software or process.

Ismail also sees this as an area of increasing relevance and, from an actuarial perspective, thinks there are some pretty important gray areas that need to be clarified.

“As carriers are rolling out some of these coverages, they have to really rethink and look at the terms and conditions and say, ’Am I actually covering if you use Copilot incorrectly, and should I be covering that? Or does that sit on a different policy?’”

“That is very early on in discussions. I think a lot of people are now concerned about that, but I don’t think there’s a hard and fast rule to say, ’Look, your misuse of an AI tool should sit with this policy versus that policy,’” Ismail says.

And more than just a renewed focus on what terms and conditions stipulate, AI may open up entirely new lines of business.

The AI mania is driving an infrastructure spending boom, with “hyperscalers” rushing to build out data centers, some of which can cost tens of billions of dollars to build.

This is driving a surge in specialized consulting. Marsh recently launched a specialized advisory group to advise clients on digital infrastructure buildouts.

Insuring data centers at this scale means answering novel questions about how GPUs, or graphics processing units, will be depreciated in the case of a loss, how insurers can spread concentration risk across these large, unique projects, and how to structure bespoke policies for lenders in an ecosystem where financing often occurs off balance sheet via private credit. (The ability of specialized circuits like GPUs to process enormous amounts of data makes them a critical component in data center buildouts.)6

Insuring obscure financing deals that ultimately fund the plumbing of AI is one thing, but on the software end, the newest generation of frontier AI models could pose even more abstract challenges to traditional loss assumptions on the cyber side.

For example, Anthropic’s newest model, Mythos, reportedly has such powerful autonomous coding capabilities that its release, as of April, has been withheld from the public due to fears that it could exploit vulnerabilities faster than companies can fix them.

Mozilla said7 it used the program to find and fix some 271 bugs in its Firefox browser; banks are rushing to gain access to the program; global regulators8 are examining the risks it could pose to the financial system; and Anthropic’s CEO went to the White House9 to discuss Mythos and cybersecurity concerns the model may bring to light.

Five years out

For brokers, “the assets are in the elevators; they’re people,” Dolin-Benguigui says. And, for commercial lines especially, it’s still very much a people business.

She also sees another advantage for brokers in the current market: the pricing cycle. She believes the insurance industry is entering a soft market — one that she thinks may last for a while — and with insurers competing more fiercely, they’ll need distribution from brokers.

So, how does the job of the broker look five years from now?

For Shields, even given the pace of innovation in AI, he thinks the industry will simply be incrementally more efficient — not fundamentally different.

Longer term, however, it could be a very different story, although it will follow a familiar theme: consolidation. “The difference between AI-enabled and non-AI-enabled companies in 20 years is going to be so dramatic that smaller companies will really struggle,” he says.

What about actuaries? What does all this mean for them?

For Dolin-Benguigui, she’s not overly sanguine about the job security. She advised her 18-year-old niece, who’s good at math, to study to become an actuary. But given the prominence of AI, her niece was afraid there wouldn’t be a role for her.

“So I think actuaries should be afraid for their jobs,” Dolin-Benguigui says. “I would advise actuaries to try to hone their skills and think of ways that they could add value in a world where the more scalable, repeatable kinds of tasks could be replicated by AI.”

For Ismail, however, she sees all this as invigorating for the profession.

Take reserving actuaries: She anticipates less of a focus on building out reserving techniques and more of a focus on the “explainability of why the results are the way they are, and how do you actually act on them?”

“I think it’s super exciting, because that’s why people become actuaries, right? You’re not really focused on the data cleansing aspect or the operational aspect. You want to focus on the insights and the next steps.”

She sees AI as “a multiplier for brokers and actuaries,” saying that technological innovation is “just a very exciting opportunity to get more integrated with AI, use it more on a day-to-day basis, and just because it changes your role it doesn’t mean it’s something to shy away from.”

Sure, the actuarial profession needs to adapt and change with the times, but it’s not exactly on weak footing. The Bureau of Labor Statistics sees the number of actuarial jobs growing by 22% between 2024 and 2034, “much faster than the average for all occupations,” according to the agency.10

In fact, there’s reason to believe that the next five to 10 years wind up being some of the most exciting in the profession’s history, as actuaries are freed up to do more risk architecture and big-picture strategy.

The February sell-off priced in the death of a business process, not the death of the insurance broker business. And while declines in many leading broker stocks were steep, markets didn’t even glance under the hood at how the headline event — an insurer offering quotes directly in ChatGPT — quickly ran into usability speedbumps.

And while ChatGPT may be learning how to talk shop, it’s the human architect who still has to navigate the world that the policy actually protects.

- https://finance.yahoo.com/quote/%5ESP500-4030/history/.

- https://www.marshberry.com/eu/blog/is-ai-rewriting-the-rules-of-insurance-distribution-and-valuation/.

- https://www.insurtechinsights.com/openai-approves-first-insurer-built-ai-app-on-chatgpt/.

- https://leg.colorado.gov/bills/sb21-169.

- https://content.naic.org/committees/h/big-data-artificial-intelligence-wg.

- https://www.cnbc.com/2026/04/06/ai-data-centers-financing-insurance-deals-gpu-debt.html.

- https://www.wired.com/story/mozilla-used-anthropics-mythos-to-find-271-bugs-in-firefox/.

- https://www.reuters.com/business/finance/banks-close-contact-with-european-regulator-anthropics-mythos-banker-says-2026-04-20/.

- https://thehill.com/policy/technology/5843290-anthropic-mythos-white-house/.

- https://www.bls.gov/ooh/math/actuaries.htm#tab-6.

Developing News

The TRIA Challenge Revisited

he Terrorism Risk Insurance Act (TRIA) program, set to expire on December 31, 2027, is receiving bipartisan1 support for another seven-year extension. The federal terrorism insurance backstop was designed for physical terrorism, but a key question now is whether it can realistically function as a backstop for catastrophic cyberterrorism. Early legislative activity in both chambers creates an opportunity for a broader debate about the adequacy of TRIA’s certification framework in an era of rapidly evolving cyber risk.

The TRIA Program Reauthorization Act of 2026, or H.R. 7128, is moving through the House2 and is largely similar in structure to its 2019 incarnation. Other than technical changes, the new bill would require the Secretary of the Treasury to publish notice that the process to certify an event as an act of terrorism has begun within 30 days following the occurrence and that any final certification determination will be issued within 90 days of that publication. Additionally, the minimum property and casualty losses necessary to certify an act would increase from $5 million to $10 million in 2029.

A proposed amendment in the House Financial Services Committee would have shortened the extension to five years, increased the program trigger from $200 million to $250 million, decreased the federal cost share from 80% to 70%, and required a study on charging insurers an annual participation fee. The amendment was voted down 49-2, suggesting that further limiting TRIA’s potential exposure for taxpayers is not a priority in the House legislative process at this time. With that broader debate largely sidelined for now, attention is also turning to a related question — how should TRIA be expected to respond to cyberterrorism losses?

The 2019 reauthorization required the Government Accountability Office (GAO) to study insurance coverage for cyberterrorism. In its 2025 report, the GAO concluded that while TRIA could theoretically apply to terrorism losses under eligible cyber policies, cyberterrorism events may not readily satisfy TRIA’s certification criteria. The report highlighted several practical hurdles.3 Many cyberattacks (1) may not meet TRIA’s requirement that an act be violent or dangerous to human life, property, or infrastructure, (2) may not clearly meet the requirement that the act be committed to coerce the US population or government or influence policy, and (3) may raise complications regarding TRIA’s geographic damage requirements. For that reason, the GAO suggested that if Congress considers a federal cyberterror insurance response, it may need to be structured as a program distinct from TRIA with clearer triggering criteria. The GAO also emphasized that any such federal response should incorporate features that mitigate moral hazard, such as cybersecurity requirements or incentives that encourage insureds to invest in stronger controls.

What this means for actuaries:

Please see the September/October 2014 and January/February 2020 Actuarial Review for previous coverage of TRIA.

Developing News

The Middle East Conflict: Impacts on P&C Insurance

This is an update to “Middle East Tensions: Impact of Geopolitics on Marine Commercial Insurance” published in Sept/Oct 2025.

he conflict in the Middle East, which began in late February 2026, has created a “perfect storm” in the global commodity market and has disrupted naval traffic through the Strait of Hormuz. The narrow water passage is a major choke point for one-fifth of the international trade of oil and gas.1 Shipping vessels were left stranded in the Persian Gulf under threat of attack and denied safe passage to their home bases. On the ground and in the air, strikes caused severe damage to major infrastructure in the region.

The exact impacts of the conflict will largely depend on how long naval shipping through the Strait of Hormuz remains blocked and the extent of damage incurred to the infrastructure in the Middle East. The increase in oil and natural gas prices directly impacts the transportation industry, driving up construction material, equipment, and machinery replacement costs. Economists estimate that every $10 per barrel increase in the price of crude oil would add approximately 0.2 to 0.3 percentage points to the consumer price index (CPI).2 Supply chain disruptions also contribute to an inflationary environment as parts manufacturing, shipping, and labor costs are dependent on energy inputs.

The increase in energy prices could cause drivers and shippers to seek alternative modes of transportation and governments to shift their investments toward renewable energy sources. Countries that supply oil and natural gas, such as the U.S. and Canada, will not be as hard hit by energy inflation as other countries that depend fully on oil supplied by the Middle East.3

What this means for actuaries:

While higher energy prices contribute to inflation and increased costs, it may also prove to be a blessing for insurer investment returns. Fixed income portfolios would benefit from higher interest rates in the short to medium term. Additionally, since most insurance policies have war coverage exclusions, the claims impact likely would not be significant, especially if the conflict is short-lived.

Further impacts will vary depending on the underlying products being written. For standard risks, actuaries can start by scenario testing various inflation rate scenarios in preparation for potential inflation if oil price spikes persist. Otherwise, a more measured strategy of “wait-and-see” is effective during these times of high uncertainty.

- https://www.weforum.org/stories/2026/04/middle-east-war-iran-us-ways-countries-respond-oil-energy-shock/.

- https://www.investopedia.com/ask/answers/06/oilpricesinflation.asp.

- https://canadianunderwriter.ca/news/industry/what-the-gulf-war-means-for-canadas-pc-insurance-industry/?utm_source=newcom&utm_medium=email&utm_campaign=CanadianUnderwriterNative&hash=7576A0101045I6L&oly_enc_id=7576A0101045I6L.

- https://www.businessinsurance.com/insurers-cancel-war-risk-cover-amid-iran-conflict/.

- https://www.insurancebusinessmag.com/nz/news/breaking-news/the-iran-wars-hidden-insurance-crisis-570337.aspx.

Developing News

CAS and SOA Publish 2026 Emerging Risks Survey

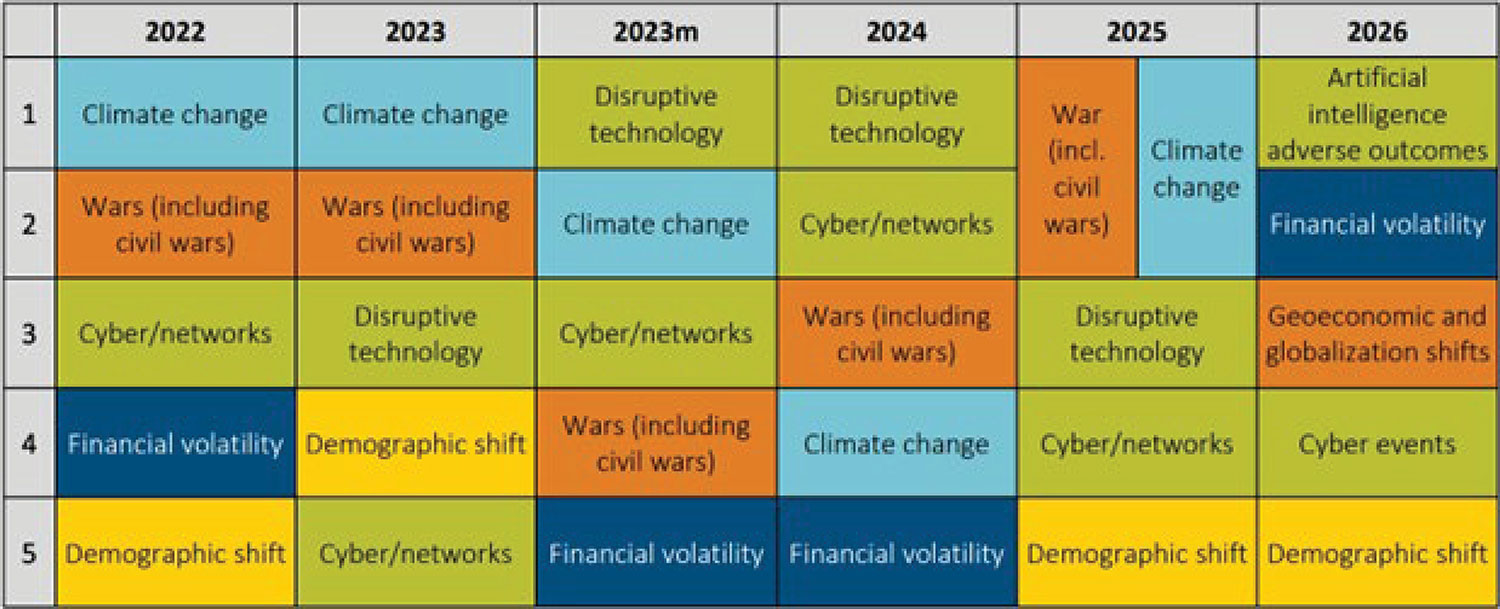

he Casualty Actuarial Society and Society of Actuaries Research Institute released results from their 19th Annual Survey of Emerging Risks in March 2026. Conducted in January with 350 risk management professionals across insurance and financial service companies, the survey asked respondents to rank 17 risks spanning economic, environmental, geopolitical, societal, and technological categories.

The 2026 ranking includes several shifts from prior years. Artificial intelligence adverse outcomes topped the list, followed by greater-than-normal financial volatility, geoeconomic and globalization shifts, cyber events, and demographic shifts. Disruptive technology has been a top-three risk in past surveys, a concern that has narrowed focus to AI in 2026. Climate change, a top-five fixture every year since 2022, dropped off the list. Environmental risks remain significant but may simply be shifting from emerging threats to embedded, managed exposures. Wars (including civil wars), which led the 2025 ranking, also dropped out, though responses came in “during various buildups in the Persian Gulf area, but well before the start of the current conflict there around Feb 28,” says R. Dale Hall, managing director of research at the SOA. Geoeconomic and globalization shifts took the place of armed conflict in the 2026 survey.

The survey includes a detailed breakdown for C-suite respondents, drawing from over 100 chief risk officers, chief actuaries, and other senior thought leaders. C-suite respondents came from a variety of industries, including life, P&C, and consulting. When asked to pick the single most impactful risk for 2026, the C-suite group landed on financial volatility (25%), followed by geoeconomic shifts (19%), and extreme weather events (14%). At the category level, 34% of C-suite respondents identified an economic risk as most impactful, and 26% identified a geopolitical risk.

What this means for actuaries:

- Casualty Actuarial Society and Society of Actuaries Research Institute, 19th Annual Survey of Emerging Risks, March 2026. https://www.casact.org/sites/default/files/2026-03/19th-Emerging-Risk-Survey.pdf.

- Casualty Actuarial Society, “Economic and Geopolitical Risks Top C-Suite Concerns in Emerging Risks Survey,” March 10, 2026. https://www.casact.org/article/economic-and-geopolitical-risks-top-c-suite-concerns-emerging-risks-survey.

Developing News

Does Project Glasswing Expose P&C Industry’s Glass Jaw?

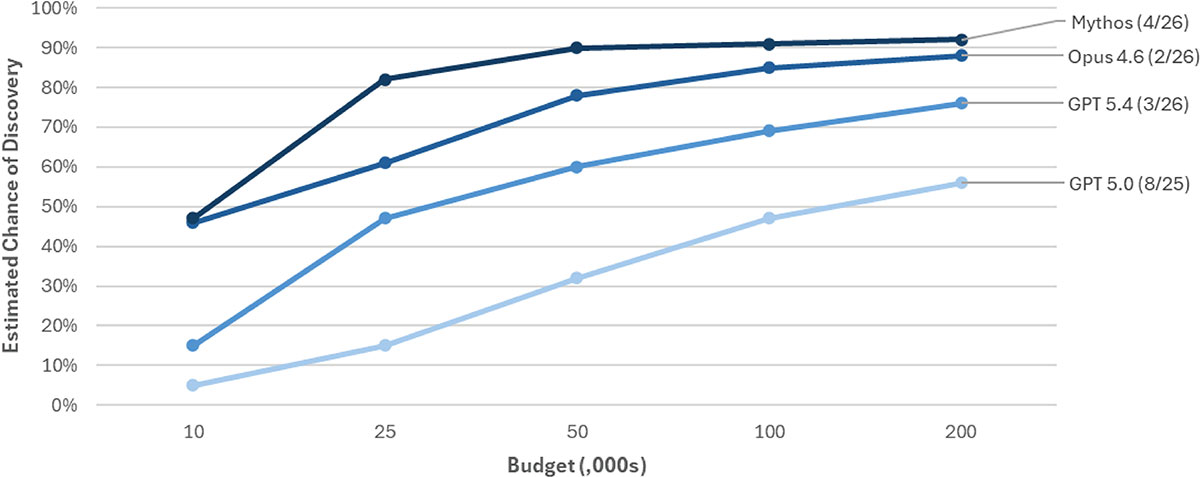

n early April, Anthropic made headlines with reports that its latest AI model, Mythos Preview, “has already found thousands of high-severity [cyber] vulnerabilities, including some in every major operating system and web browser.”1 The model identified and crafted exploits for vulnerabilities unscathed by decades of security research. Anthropic subsequently launched Project Glasswing in collaboration with over 50 companies, such as Amazon, Apple, and Google, to help fortify their defensive postures using the Mythos Preview. Mythos may be a warning sign for a market defined by “sustained softening,”2 but opinions remain divided regarding whether it represents a true step change in offensive capability.

Some security experts say much of Mythos’s discovery capability was already available through savvy orchestration3 of existing models for months if not a full year. Offensive security platform XBOW, which was invited by Anthropic to evaluate Mythos, found that it significantly outperforms predecessors in discovering “validated, actionable vulnerabilities in live website environments.”4 Figure 1 displays the estimated chance of discovery based on XBOW’s report at various output token budgets.5

At higher budgets, the models begin to converge, especially between Mythos and its direct predecessor, Opus 4.6.

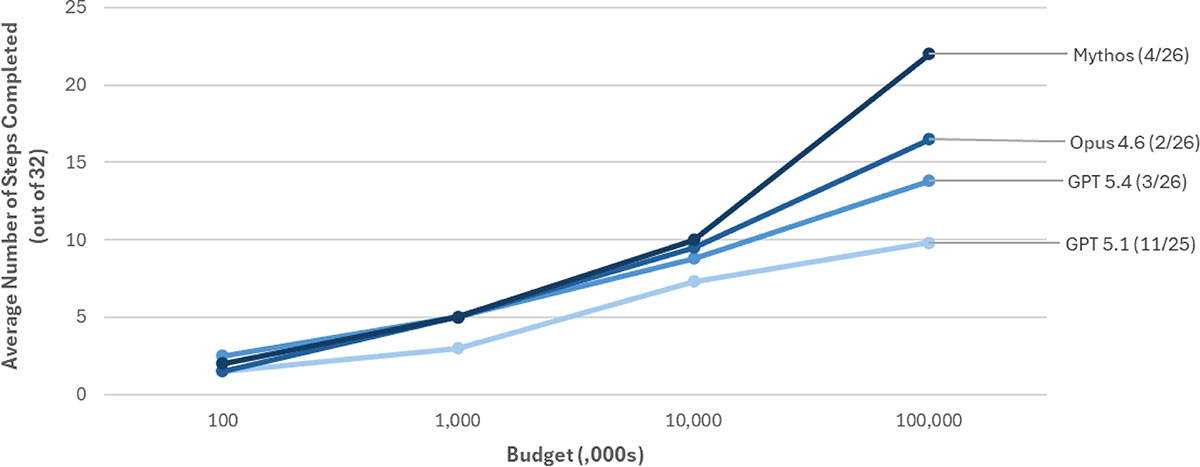

Mythos’ exploitation capabilities appear to be more novel than its discovery capabilities. AI Security Institute (AISI) found that Mythos succeeded in 73% of expert-level6 identification and exploitation tasks — tasks that no model could complete before April 2025. Mythos succeeded three out of 10 times and completed an average of 22 out of 32 steps of The Last Ones (TLO) corporate network attack simulation. Figure 2 compares Mythos’s performance to that of other models at different token consumption.7

While no other model completed TLO at any budget, Mythos’ successful completion required multiple tries and extensive computational resources. Other models achieved results similar to that of Mythos in lower budget ranges. AISI credited Mythos for its strong autonomous attacking capability against weakly defended systems but “cannot say for sure whether Mythos Preview would be able to attack well-defended systems.” Project Glasswing itself illustrates a growing viewpoint that AI may empower defense8 more than offense.

What this means for actuaries:

Actuaries may consider revisiting frequency assumptions both generally and within catastrophe models, particularly where upstream points of failure, such as Amazon Web Services or Microsoft Azure, have contributed to recent near-miss cyber aggregation events.13 Vulnerability and resilience covariates14 may also assume greater importance in pricing and exposure models.

- https://www.anthropic.com/glasswing.

- https://www.reinsurancene.ws/cyber-insurance-market-enters-critical-phase-amid-softening-rates-and-rising-exposure-dual/.

- https://www.cnbc.com/2026/05/08/anthropic-mythos-ai-cybersecurity-banks.html.

- https://xbow.com/blog/mythos-offensive-security-xbow-evaluation. XBOW defines actionable as a validated way to act on the vulnerability after a series of 80 actions.

- The author started with XBOW’s graph “finding web vulnerabilities in OSS with fixed token budget,” extracted points, converted the y-axis from odds to likelihood, and interpolated as needed to produce this graph.

- https://www.aisi.gov.uk/blog/our-evaluation-of-claude-mythos-previews-cyber-capabilities. The author started with AISI’s graph “completed steps on The Last Ones per spent tokens,” extracted points, and interpolated as needed to produce this graph.

- https://www.aisi.gov.uk/blog/our-evaluation-of-claude-mythos-previews-cyber-capabilities. The author started with AISI’s graph “completed steps on The Last Ones per spent tokens,” extracted points, and interpolated as needed to produce this graph.

- https://www.belfercenter.org/sites/default/files/2026-03/ISEC.a.398.pdf.

- https://ar.casact.org/ai-generates-single-point-of-failure-rethink/.

- https://beinsure.com/ransomware-evolution/.

- https://digital.casact.org/issue/may-june-2026/the-stem-hero-at-the-front-lines-of-the-ai-revolution/.

- https://insights.cybcube.com/en/cyber-insurance-in-the-age-of-claude-mythos.

- https://ar.casact.org/amazon-aws-and-microsoft-afd-outages-pcs-latest-cyber-kitty-cat-events/.

- https://www.insurancebusinessmag.com/uk/news/cyber/cyber-insurance-improves-but-gaps-remain-575275.aspx.

Insuring Solar Storms: Modeling Considerations for Space Weather Risks in Insurance Contracts

eomagnetic storms, or solar storms, were previously thought to be a concept from dystopian science fiction. More recently, they have been considered an emerging risk in the insurance industry. Solar storms are nothing new, so why are they an emerging risk now?

The largest documented storm (the Carrington Event of 1859) knocked out the biggest communication system of the time, the telegraph system. We live in a much more plugged-in, energy-dependent world now, with new data centers being planned to support our increasing dependence on artificial intelligence. As this dependence grows, the next Carrington-level event would have far more severe consequences.

While some may be of the opinion that geomagnetic storms are not insurable, these events, or the physical phenomena they can create, do meet the technical criteria for insurable risks: Geomagnetic storms are not speculative; they are due to chance; they can lead to definite and measurable losses; and they are statistically predictable. The potential for truly catastrophic outcomes, however, raises legitimate concerns about how such risks should be underwritten and managed.

That being the case, technical insurability does not always imply strategic insurability. A risk,1 even backed by sound actuarial pricing, might not be the most efficient allocation of an insurer’s capital. This paper addresses insurability concerns of solar storms and presents modeling and underwriting considerations.

Geomagnetic disturbance (GMD)

It is important to note that electromagnetic incidents can occur due to both natural and man-made causes. Natural causes include lightning strikes or severe solar activity (e.g., solar wind, solar flares, solar energetic particles (SEPs), or coronal mass ejections (CMEs)). Man-made causes include nuclear weapon detonation (either above or below atmosphere) or a non-nuclear radio frequency weapon. This paper focuses exclusively on naturally occurring events.

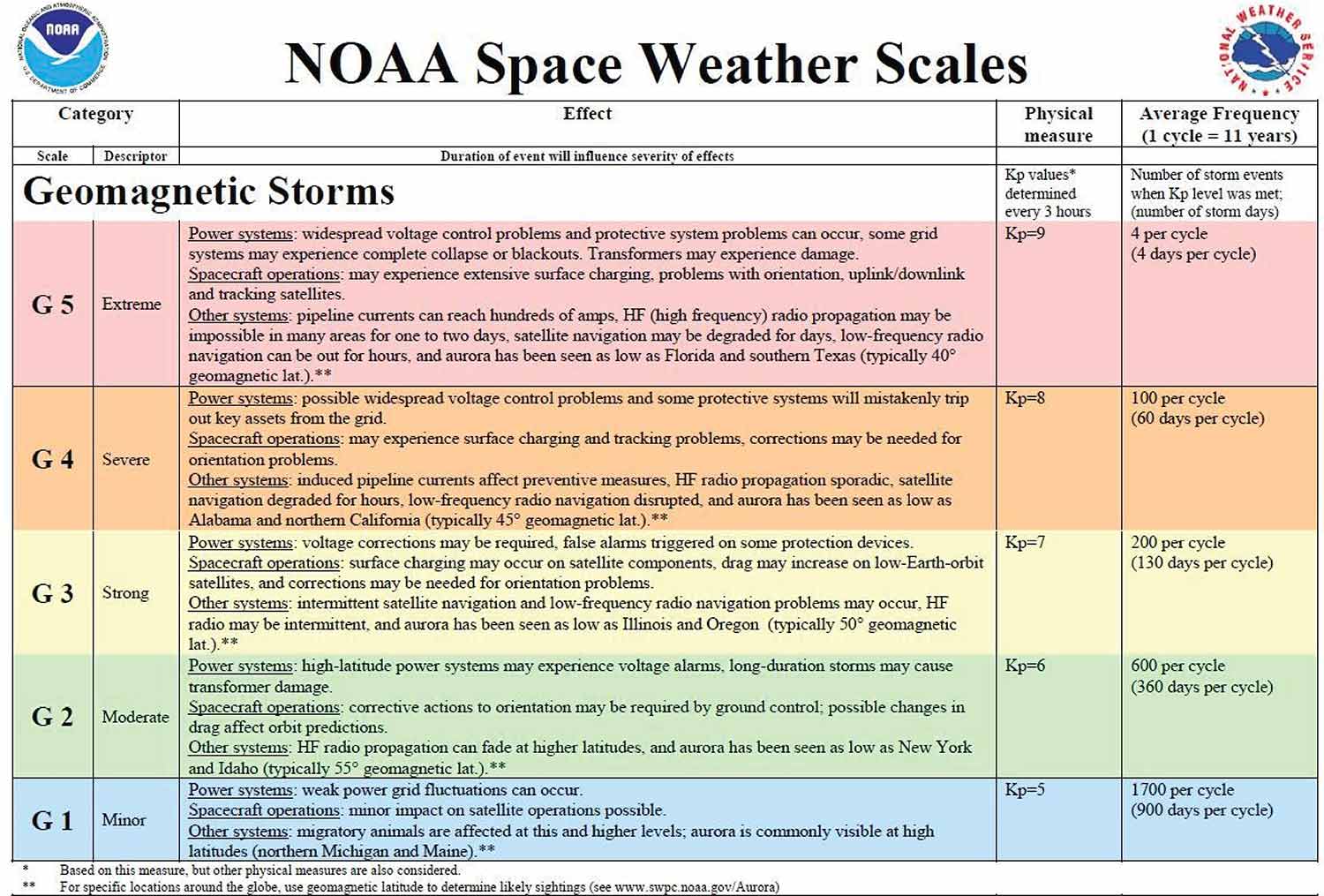

As with hurricanes, geomagnetic storms can be characterized using established intensity scales, several of which can serve as the basis for insurance triggers. Common indices include:

- Kp index published by the GFZ Helmholtz Centre for Geosciences.

- Ap4 (a derivation of Kp index).

- Dst (Disturbance Storm Time Index)4 maintained by the NOAA National Centers for Environmental Information. The Dst is expressed in nanoTeslas (nT), where the lower the value, the greater the intensity of the geomagnetic storm.

Figure 2 categorizes geomagnetic storms into five broad categories (G1 to G5) based on the storm’s Kp index. This is not dissimilar to the Saffir-Simpson Hurricane Wind Scale, which rates a hurricane’s intensity from 1 to 5, as defined by sustained wind speed.

Notable historical geomagnetic disturbance events

Subsequent notable events have continued to demonstrate the disruptive power of geomagnetic storms, especially as reliance on electrical and communication systems has grown. The 1921 New York Railroad Storm, for example, sparked multiple fires and again knocked out telegraph systems in both the U.S. and Europe. The event also impacted transatlantic cables, and while its intensity, –907 nT,7 was greater than that of the Carrington Event, and therefore less severe, its destructiveness was amplified by the increased dependence on electricity.

More recently, the 1989 Quebec storm led to the failure of the Hydro-Quebec power grid, resulting in a nine-hour blackout that affected millions. The storm also caused power transformers in New Jersey to melt, further evidencing the vulnerability of modern infrastructure. The intensity for this event was recorded at –589 nT.8

Advancements in technology have introduced new domains of risk, particularly in aviation and satellite operations. The 2003 Halloween Space Weather Storms required flights to be redirected to avoid elevated radiation levels, while Earth-orbiting satellites suffered data outages and some were temporarily lost. Although the measured intensity of this event, –401 nT,9 was greater than the 1989 Quebec storm, the consequences for aviation and telecommunications were significant. This expanded impact domain demonstrates the evolving nature of geomagnetic storm risk as society becomes increasingly dependent on complex technological systems.

Modeling of geomagnetic storm risks

Frequency

While these events may sound more like science fiction, a Carrington-level solar storm has an estimated return time similar to that of a magnitude 7.5+ earthquake in the continental U.S. A Quebec-level solar storm has an estimated return similar to that of a category 5 hurricane making landfall in the U.S.

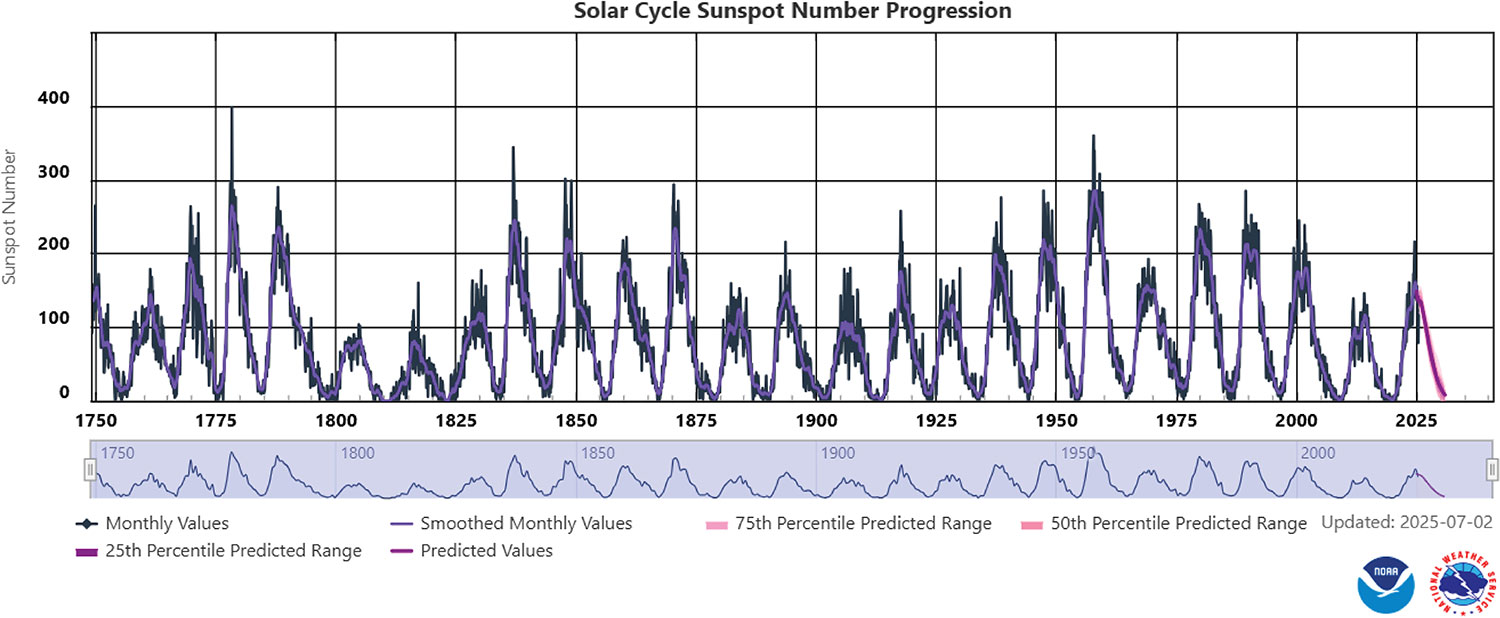

Scientific methods employed to estimate the likelihood of geomagnetic storms vary in approach and conclusion. However, scientists across the board agree that the likelihood of geomagnetic storms can vary based on where we are in the solar cycle. The solar cycle lasts approximately 11 years and captures the rise and fall of geomagnetic activity on the sun’s surface. Assuming an annual insurance policy, where those 12 months fall in the solar cycle can be determined by counting the number of sunspots.10 As a result, frequency for two policies may differ if they are at different periods of the 11-year cycle (see Figure 3).

During periods of high sunspot counts, the solar cycle is in an “active” period and the likelihood of geomagnetic storms increases. Historical and forecasted sunspots are available from various observatories. Given a policy period, insurers can reference the forecasted sunspot counts to determine the activity level and subsequently the likelihood of an event.

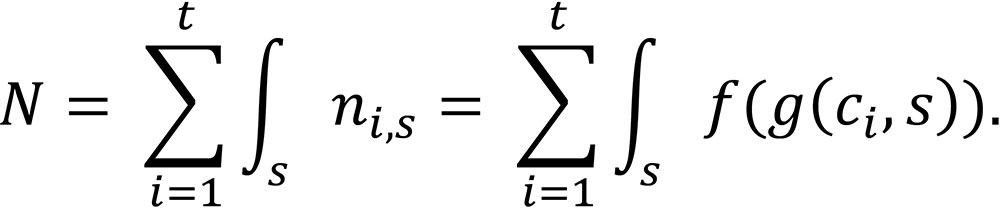

Let λi,s be the frequency parameter(s) for each month i of the policy for a given geomagnetic storm intensity, s (e.g., nT). Additionally, ci is the monthly sunspot count for month i.

λi,s = g(ci,s)

With this approach, λ = g(c,s) is selected to be an increasing function of sunspot count and a decreasing function of geomagnetic storm intensity. Intuitively, this captures the increase in storm likelihood during a more active period and the lower likelihood of a larger storm happening, all else being equal.11

(dλ/dc)≥0, (dλ/ds)≤0

Let ni,s be the total simulated storm count of size s in month i:

ni,s ~ f(λi | ci,s), where f is the selected discrete probability distribution.

Let N be the total simulated solar storm count in a particular Monte Carlo iteration. Also, let t be the duration of the insurance contract in months (in most cases, assume t = 12). There are limited studies into event dependence, with some existing literature suggesting a relationship between probability of a large geomagnetic storm and time since the last event. Assuming s is a continuous measure of storm intensity (e.g., nT), the low event probability allows us to reasonably assume

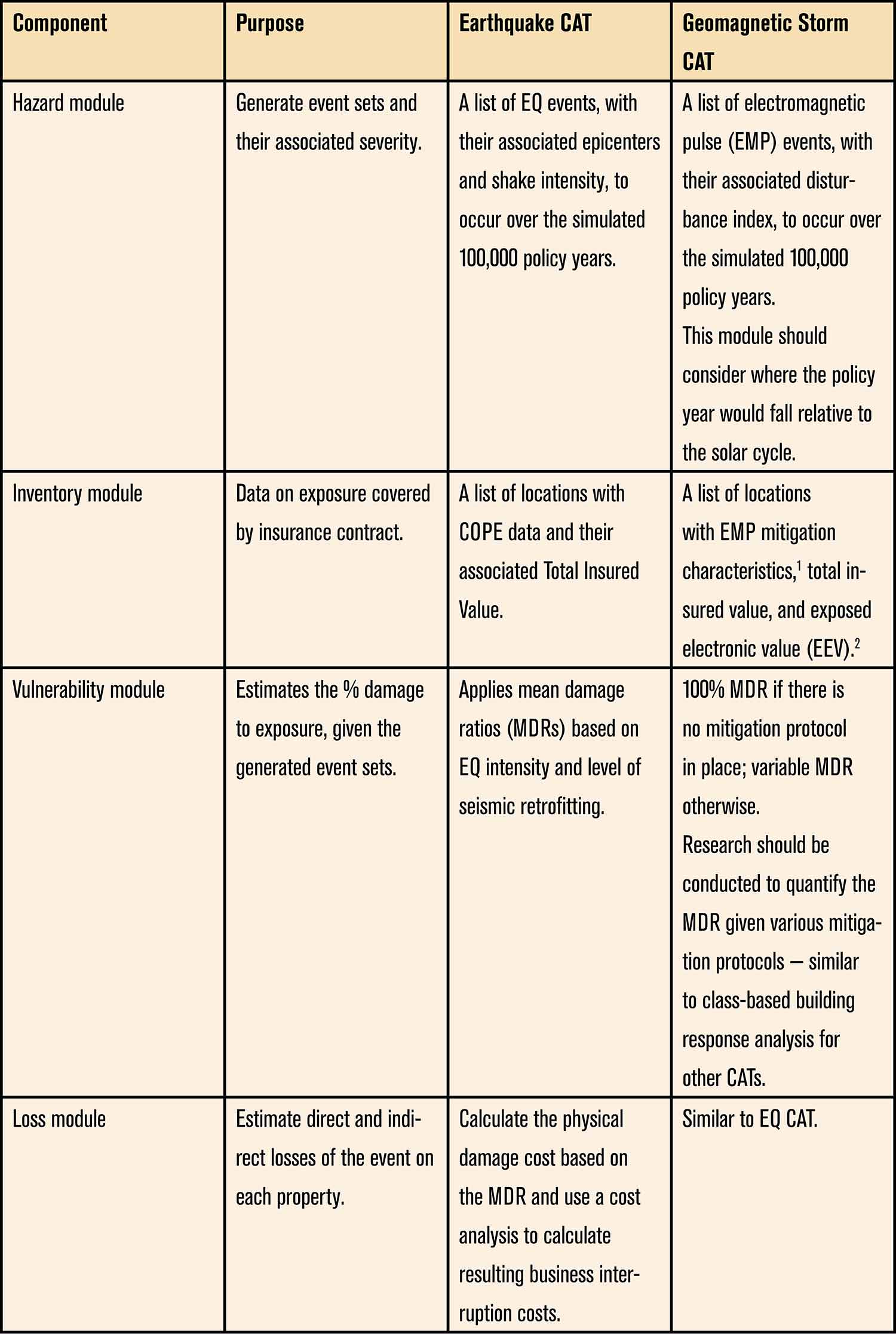

Catastrophe (CAT) model for geomagnetic storms

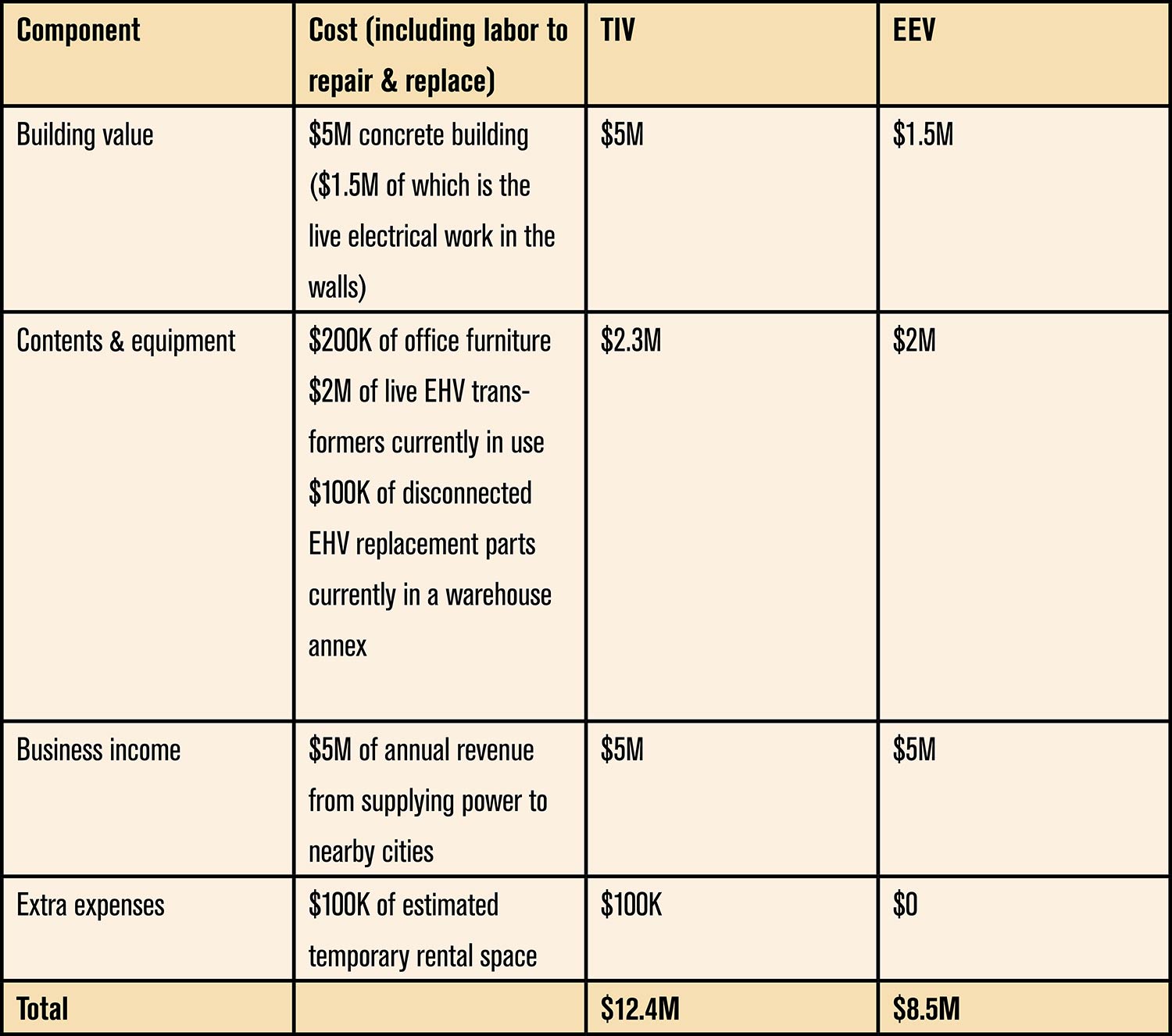

Total insured value (TIV) vs. exposed electronics value (EEV)

The most direct risk of geomagnetic storms is severe damage to electronic equipment and infrastructure. For example, extra high voltage (EHV) transformers can be permanently damaged following a geomagnetic storm. As of 2014, over 2,300 EHV transformers can be put at risk in the U.S.12 Unlike other catastrophe perils, the physical risk to nonelectrical equipment is low.13 Using TIV will overstate the exposure directly vulnerable to geomagnetic storms and subsequently overstate the capital needed to underwrite the risk. This paper suggests quantifying EEV using the following equation:

Exposed Electronics Value

= Total Insurable Value — Nonelectrical Building Value

— Nonelectrical Contents & Equipment

— Disconnected Electrical Contents & Equipment

Consider the exposure of a power plant in Table 2.

Current geomagnetic storm coverage in insurance contracts

A standard commercial property insurance policy does not explicitly exclude damage due to a geomagnetic storm. Property insurance may cover property damage and business income losses in the event of a loss due to a covered peril. For example, a fire starts because of a power surge from a geomagnetic storm. Assuming geomagnetic storm is not an explicitly excluded peril, a standard property insurance would pay out for the physical damage, as well as the corresponding business interruption.

A business may need to consider specific coverage or potentially available coverage under other policies, such as cyber (data loss or electronic disturbance), equipment breakdown (damage to electrical systems), or business interruption (due to power grid failure). These still may leave gaps in coverage for a business with significant electrical infrastructure.

- While not dicussed in detail in this paper, example strategies include blocking capacitors and electromagnetic shielding (e.g., Faraday cages).

- See Total Insured Value (TIV) vs. Exposed Electronic Value (EEV) section.

Issue #1: Remote electrical infrastructure

Issue #2: Business interruption gap

As a practical metric for structuring a parametric policy, the NOAA Space Weather Scales can be referenced. The similarity to more familiar weather scales, such as the Saffir-Simpson hurricane category system, could aid in the underwriting and explanation of coverage triggers.

Issue #3: Aggregation risks for insurers and reinsurers