Navigating Risk and Fairness in P&C Insurance with Algorithmic Auditing

raditional statistical frameworks have long anchored the U.S. P&C insurance industry, but mounting pressures around social equity and data-driven decision making are forcing shifts in how risk is assessed and in how policies are shaped. At the recent CAS 2026 Spring Meeting, the session, “Making a Greater Impact: Expanding the Role of Actuaries in Today’s Critical Issues,” explored how professionals can move beyond conventional boundaries to address pressing socioeconomic challenges. The presentation featured Cathy O’Neil, a mathematician, data scientist, author, and CEO of ORCAA, an algorithmic auditing firm. O’Neil challenged insurers to rethink the definition of “fairness” in an era of granular data and to translate these values into proactive participation in affordability and availability solutions for all of society.

Analytical choices in research

O’Neil argued that while “omitted variable bias” is the technical explanation for this paradox, the real issue is the human tendency to seek overly simplistic explanations. When we resist this tendency, we can recognize that both the high-level disparity and the department-level parity are “true” statements depending on the context. For insurance professionals, the key takeaway is that context is paramount, as omitting relevant variables can lead to misleading conclusions about bias and risk.

This variability underscores both the challenge and opportunity of auditing models. Rather than viewing inconsistent outcomes as meaningless, auditing models use such outcomes to develop a set of guiding principles for making and interpreting the analytical choices behind them. Every model is essentially a series of questions:

- For whom does this algorithm work?

- In what context does it cause harm?

- What constitutes a “reasonable” form of discrimination in a risk-based industry?

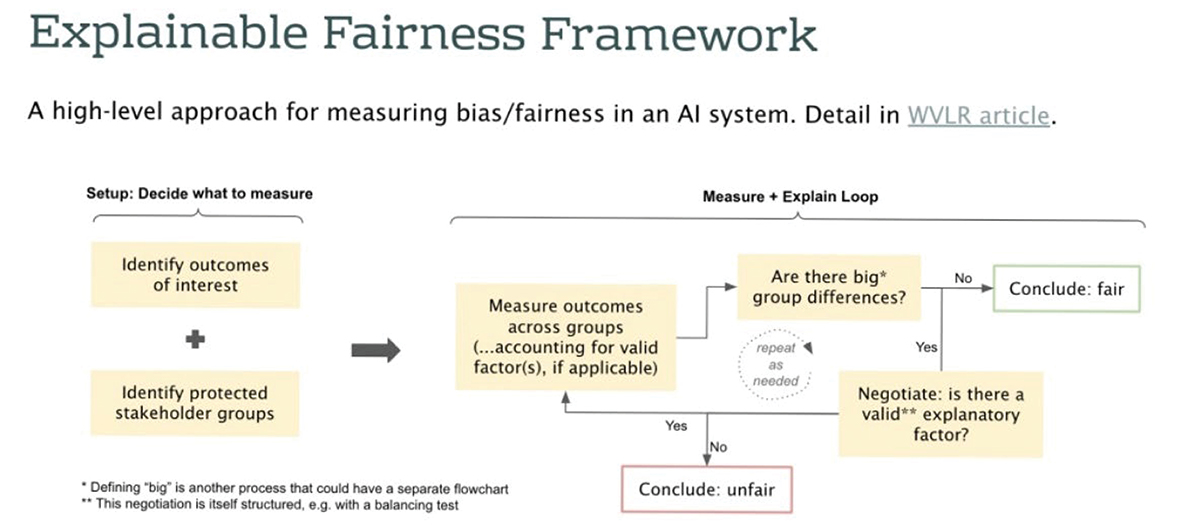

The explainable fairness framework

- Setup: Outcomes of interest (such as insurance premium) and protected stakeholder characteristics (such as sex) are identified.

- Measure: Differences in outcomes across these protected groups are calculated, also referred to as the “gap.”

- Evaluate: Oversight and regulatory entities evaluate this gap. If they deem the gap acceptable, they conclude the system is “fair.” If it is considered significant, the parties move to the “negotiate” phase.

- Negotiate: In this phase, algorithmic operators (i.e., private companies) identify if there are valid explanatory factors to justify the gap.

- The loop: If an explanatory factor is accepted as legitimate, the framework loops back to the “measure” phase to recalculate the gap while accounting for the new factor. If the algorithmic operators fail to provide explanatory factors and a significant gap remains, the oversight entities conclude the system is “unfair.”

O’Neil described the result of this process as a “dial” that can be monitored in an algorithmic “cockpit,” or dashboard, providing a clear explanation of how fairness may be defined and maintained in a specific context.

Case studies in insurance and lending

Student majors and loan outcomes

For student lending, outcomes of interest might include loan approval, interest rates, or penalties for late payments. When a race-based gap in interest rates was determined to be present, the negotiation involved identifying explanatory factors like the student’s major or their college ranking as legitimate reasons to charge more. These disparities raise ethical questions about whether it is appropriate to penalize students based on their chosen field of study, which may be influenced by college-led strategies to optimize graduation rates.

Disability insurance

For disability claims, the focus shifts to approval rates and the length of the initial claim. While FICO scores might be legitimate in a lending context, it is likely inappropriate for disability insurance. Instead, factors like age, comorbidities (such as diabetes), and the type of injury are typically regarded as better tied to the risk of prolonged recovery.

Personal auto insurance

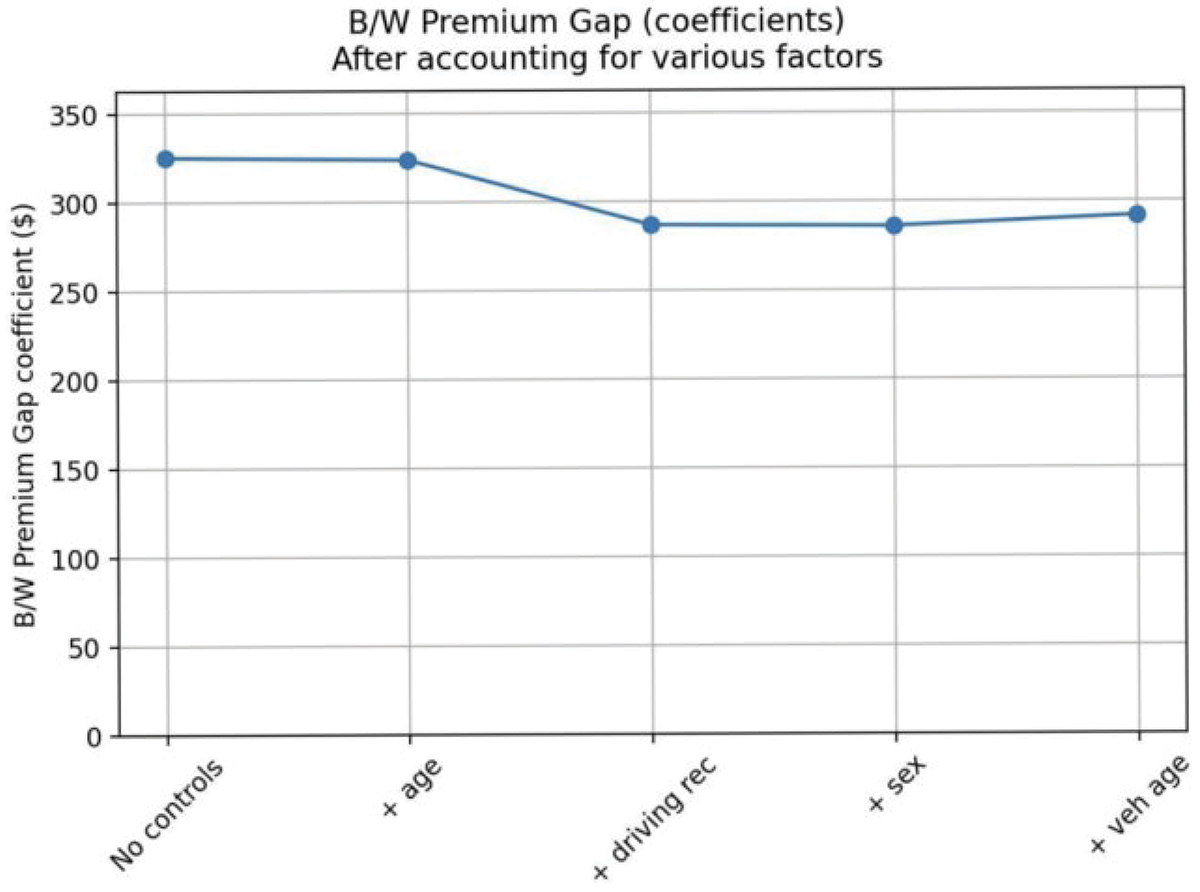

O’Neil delved deeply into the complexities of auto insurance, questioning whether current rating systems could be perceived as having a disparate impact on minority drivers. The explainable fairness framework indicated significant premium gaps between racial groups. While some of these gaps can be explained by legitimate factors such as driving records, the framework revealed that the gap often remains robust even after accounting for age, vehicle type, and gender.

O’Neil noted that judges and regulators often prefer factors that are under the control of the individual or are directly related to risk. Negotiations tend to center on whether factors like geography and credit-based insurance scores should be grandfathered in as legitimate, or if they act as proxies for historical inequalities like redlining.

Uncovering historical bias

Although the Fair Housing Act of 1968 addressed redlining, it was interpreted at the time to not apply to insurance practices. The law’s application to insurance was not explicitly clarified until the 1989 Housing and Urban Development (HUD) Final Rule on the Fair Housing Amendments Act of 1988, which was not confirmed through federal courts until 1992. Today, this legacy remains a challenge for the insurance industry, as modern rating factors like ZIP codes, FICO scores, and geography can act as statistical proxies for these redlined areas, potentially contributing to persistent premium disparities between racial groups.

In the past, a lack of granular data necessitated a shared societal risk approach by default. However, through technological innovation and an abundance of big data, there now exists the ability to model risk at granular levels, potentially making insurance unaffordable for those who need it most. O’Neil advocated for the industry to embrace innovative risk management systems that balance individual risk modeling with the public good of a functioning insurance system, which aligns with the fundamental insurance principle of spreading risk across society.

The CAS has demonstrated significant leadership in this space through a series of research papers examining potential bias in insurance pricing and related practices. These publications can help guide the insurance industry toward proactive, quantitative approaches for promoting fairness. Using these resources, professionals can ensure the industry continues to grow, to adapt, and to shape a future that serves the public good.

Fairness is an entirely contextual, often temporary, and fundamentally normative cultural phenomenon. However, the continuity of these norms across time proves that equity evolves according to an underlying rationale rather than due to arbitrary shifts, providing a stable foundation to be managed professionally. Because this logic exists, actuaries have a unique opportunity to lead the conversation on how fairness is defined and maintained. The path forward entails:

- Active participation: Actuaries should lead the conversation on how fairness is defined rather than waiting for external mandates.

- Robustness and integrity: Actuaries should commit to being thoughtful about the analytical choices made in every model.

- Transparency: Actuaries should move away from black box algorithms toward explainable systems that a layperson or regulator can understand.

By engaging with these difficult questions, the insurance industry can strengthen public trust and ensure it continues to serve as a vital pillar of a resilient society.