Contents

departments

- EDITOR’S NOTE

- The Four Sides to Every Story

- President’s Message

- More Than Just a Logo

- Member News

- Comings and Goings

- Calendar of Events

- In Remembrance

- In Memoriam

- Making Things Happen

- CAS Staff Spotlight

- 2025 Annual Report of the CAS Discipline Committee Released

- CAS Discipline Committee Panel Issues Ruling

- Celebrating the 2025 CAS Volunteer Award Winners

- Professional Insight

- Developing News

- The Hidden Costs of Good Intentions: How Disaster Bailouts

- Actuarial Expertise

- Rethinking Loss Triangles for IFRS 17: How the Risk Attribution Index (RAI) Reveals the Limits of Frequency–Severity–Inflation Decomposition

- From Hype to Help: A Practical GenAI Workflow for Actuaries

- A New Way to Model Catastrophes in a Changing Climate

- Viewpoint

- Ethical Issues

- Solve This

- It’s a Puzzlement

on the cover

-

As floods become more frequent, localized, and harder to categorize, insurance coverage has failed to keep pace. This article explores why flood risk is now better understood than ever, yet still largely uninsured, and what it will take for public and private markets to finally close that gap.

As floods become more frequent, localized, and harder to categorize, insurance coverage has failed to keep pace. This article explores why flood risk is now better understood than ever, yet still largely uninsured, and what it will take for public and private markets to finally close that gap. -

What happens to property risk when buildings are printed instead of built? This article explores how 3D printed construction could reshape underwriting, resilience, and insurability — revealing both surprising risk-reduction opportunities and new challenges for property insurers.

The amount of dues applied toward each subscription of Actuarial Review is $10. Subscriptions to nonmembers are $50 per year. Postmaster: Send address changes to Actuarial Review, 4350 North Fairfax Drive, Suite 250, Arlington, Virginia 22203.

Masthead

-

Editor in Chief

Jim Weiss

-

CAS Director of Publications and Research

Elizabeth A. Smith

-

AR Managing Editor and CAS Editorial/Production Manager

Sarah Sapp

-

CAS Managing Editor/Contributor

Greg Guthrie

-

CAS Graphic Designer

Sonja Uyenco

-

CAS Cross-Functional Coordinator/Contributor

Delilah Barrow

-

News Editor

Sara Chen

-

Opinions Editor

Richard B. Moncher

-

Editors

- Colleen Arbogast

- Daryl Atkinson

- Karen Ayres

- Glenn Balling

- Robert Blanco*

- Lisa Brown

- Michael Budzisz

- Sumanth Chebrolu

- Todd Dashoff

- Daniel Jay Falkson*

- Stephanie Groharing

- Julie Hagerstrand

- Srinand N. Hegde*

- Cameron Herrmann*

- Kenneth S. Hsu

- Cindy Hu*

- Jack Huang*

- Rachel Hunter*

- Rob Kahn*

- Benyamin Kosofsky

- Julie Lederer

- Albert Lee

- David Levy

- James Li*

- Sydney McIndoo

- Stuart Montgomery

- Sandra Maria Nawar*

- Erin Olson

- Shama S. Sabade

- Michael Schenk

- Robert Share

- Craig Sloss

- Jared Smollik

- Andrew Somers*

- Bella Thiel*

- Isaac Wash*

- Radost Wenman

- Ian Winograd

- Vanessa Wu*

- Xuan You*

- Yuhan Zhao*

-

*Writing Staff

-

Puzzle

Jon Evans

-

Advertising

Al Rickard, 703-402-9713

arickard@assocvision.com -

The Casualty Actuarial Society is not responsible for statements or opinions expressed in the articles, discussions or letters printed in Actuarial Review. -

For permission to reprint material from Actuarial Review, please write to the editor in chief. Letters to the editor can be sent to AR@casact.org or the CAS Office. To opt out of the print subscription, send a request to AR@casact.org.

Images: Getty Images -

© 2026 Casualty Actuarial Society.

ar.casact.org

The Four Sides to Every Story

popular saying goes, “There are two sides to every story.” A variation goes, “There are three sides to every story — yours, theirs, and the truth.” Still another twist, attributed to Rousseau, provides: “There are four sides to every story — your side, their side, the truth, and what really happened.” The latter differentiates between facts we observe and complex realities that underlie them, while also framing stories in the shape of buildings.

Throughout 2025’s Volume 52 AR’s authors told a familiar story — unprecedented disasters, imperfect responses, fraying trust, and public sector intervention. AR presented steps the industry could take to rewrite the story — more effective regulation, product design, communication, and institutional investing. These insights targeted truth as measured in fiscal currency. March 2026’s AR dives deeper into the immeasurable.

It turns out the four-sided building metaphor implicit in Rousseau’s saying has cracks. In this issue, Vanessa Wu, ACAS, illustrates how a 3D-printed wall slab is situated amorphously in a manner analogous to soft serve ice cream. By that view, almost any story could have infinite sides. And when it comes to buildings, stories can be erected quickly and economically — potentially reshaping the dynamics of predict versus prevent.

Either way, buildings contain more substance than wood, concrete, or steel. The empathy we feel when Mother Nature tears things down inclines society to restore what it can, even as the most important things in our lives can never truly be replaced. Such empathy is not always congruent with the reality of disaster propensity. As Cindy Hu, ASA, explores in her AR feature, rebuilding in harm’s way is often the first chapter in the next tragedy.

One microcosm for the structural flaws that leave citizens exposed to danger is flood insurance in the U.S. Improved actuarial precision and a more robust private marketplace have yet to plug critical coverage gaps, as was evident in the aftermath of catastrophic Texas flooding in 2025. In his cover story, DJ Falkson, FCAS, examines the history and future of this public-private partnership. Together Vanessa, Cindy, and DJ provide three windows into a complex reality. Hopefully this gives readers a better view of what lies beneath.

Actuarial Review

Casualty Actuarial Society

4350 North Fairfax Drive, Suite 250

Arlington, Virginia 22203 USA

Or email us at AR@casact.org

More Than Just a Logo

n my previous Actuarial Review message, I highlighted a few of the CAS priorities for the 2025–26 operating year and a few of the projects I am particularly focused on as president. In this issue’s message, I am going to delve deeper into one of those projects — the refresh of the CAS brand. Before we get into the specifics of the project itself, though, it is worth taking just a minute to consider what a “brand” actually represents and why it matters.

What is a “brand?”

In other words, an organization’s brand is a function of what people believe it stands for, how they expect the organization (and its members) to behave, and how they feel when they interact with the organization and its members. So, while logos, color palettes, and taglines can all be useful in expressing and communicating a brand image, the brand exists separately from those items and has a life of its own. The CAS brand refresh project, therefore, is not so much about trying to change our brand as it is to better understand, represent, and communicate it.

Still, whenever “branding” or “brand refresh” comes up within an organization, people often have questions like:

- Is our logo going to change?

- Are we switching to new colors?

- What will this cost us?

- Why is this happening now?

Some may even think of past rebranding missteps with Cracker Barrel, Jaguar, and Bud Light and worry that changing branding strategy could create similar issues.

These reactions are perfectly natural, particularly in a professional organization like the Casualty Actuarial Society — whether you refer to it by its full name, “The C-A-S,” or CAS (pronounced “kaz”). Actuaries tend to be seen as risk-averse, highly analytical, traditional, and serious, so the idea of refreshing our brand might seem out of character. Nevertheless, after conducting market research, the CAS Board endorsed moving forward with a brand refresh, which is now well underway.

Branding reaches far beyond just logos or color schemes — it encapsulates how a professional society communicates its mission, values, and credibility. A strong, unified brand enables members, partners, and the broader community to easily understand what the Society stands for and why it makes a difference. It establishes trust, underscores professionalism, and nurtures a sense of belonging among members. In a busy environment where many groups compete for attention, effective branding helps a professional society distinguish itself with confidence, clarity, and a compelling identity that draws in others and inspires pride.

Why now?

CAS market research confirms that we are the gold standard for P&C credentialing, respected for high standards and prestige among those who know us well. At the same time, research shows an awareness and understanding gap among those less familiar with the CAS and its mission. Our strength is well established; our opportunity is to ensure that strength is clearly recognized and understood in a crowded and often noisy marketplace.

Is it worth the cost and effort?

A clear and consistent brand enhances recognition and bolsters the credibility of CAS credentials. It affirms members’ professional authority among employers, regulators, and interdisciplinary colleagues. Well-defined positioning enables stakeholders to appreciate the unique value CAS members contribute to addressing complex risk challenges, ensuring that our credential’s significance remains robust for both current members and future generations. Safeguarding and advancing the strength of the CAS credential is a fundamental responsibility of the board, which is why “Reinforcing Our Differentiated Brand” is a central pillar of the CAS Strategic Plan.

What will the brand refresh include?

The CAS is the trusted global authority advancing the practice of property and casualty actuarial science, helping people, businesses, and communities unlock opportunity and thrive in a rapidly changing world.

Over the coming year, members can expect to see a thoughtful evolution of messaging, tone, and visual identity across CAS channels, and greater consistency and clarity in how we communicate with different audiences — those who know us well and those just getting to know us. As we proceed, members should feel confident in the brand refresh effort. These decisions are grounded in market research and testing conducted by the CAS Board. The results will be informed by how members, employers, and future candidates engage with the CAS today. Members should also look forward to seeing the CAS take a modern approach to showing up in a digital-first world, while preserving the high standards, values, and mission that define the CAS.

Yes, but are we changing the logo and colors?

Closing thoughts

Actuarial Review Letters Policy

Letters shall not contain personal attacks or statements directly or implicitly denigrating the characters of individuals or particular groups; false or unsubstantiated claims; or political rhetoric. Letters should be no more than 250 words and must include the author’s name and phone number or email address, so the editorial staff can confirm the author. Anonymous letters will not be published. There shall be no recurrence of topics; issues previously addressed will not be the subject of continued letters to the editor, unless new and pertinent information is provided. No more than one letter from an individual can appear in every other issue. Letters should address content covered in AR. Content regarding the CAS Board of Directors or individual departmental policies should be directed to the appropriate staff and volunteer groups (e.g., board, working groups, committees, task forces, or councils) instead of AR. No letter that attempts to use AR as a platform for an ulterior purpose will be published. Letters are subject to space limitations and are not guaranteed to be published. The AR editorial volunteer and staff team reserves the right to edit any submitted letter so that it conforms to this policy. Decisions to publish letters and make changes to submissions shall be made at the discretion of the AR Working Group and CAS staff.

For more information on AR editorial policies, visit here.

Comings and Goings

Laura Maxwell, FCAS, MAAA, CSPA, has been promoted to principal and consulting actuary at Pinnacle Actuarial Resources. She previously served as director and consulting actuary, a title she held since 2021. Maxwell has worked in the P&C insurance industry since 1987 and joined Pinnacle in 2006. Her prior experience includes positions with a consulting firm, an automobile insurer, a state insurance department, and a national rating bureau. At Pinnacle, she leads the firm’s supervisor and professionalism key management areas. She also serves as appointed actuary for multiple insurers and collaborates with state insurance departments, captive insurance companies, and self-insured public entities. She chairs the Casualty Loss Reserve Seminar Working Group and serves as a general officer on the Syllabus and Examination Working Group at the CAS.

Calendar of Events

-

May 3–6, 2026

2026 CAS Spring Meeting

New York, NY -

May 31–June 2, 2026

2026 CAS Seminar on Reinsurance

Philadelphia, PA -

July 28–Sept 1, 2026

2026 CAS Virtual Workshop: Introduction to Python for P&C Insurance

Virtual -

September 14–16, 2026

2026 Casualty Loss

Reserve Seminar

Las Vegas, NV -

November 8–11, 2026

2026 CAS Annual Meeting

Honolulu, HI

In Remembrance

A CAS Past-President

1940–2025

CAS Past President, David Flynn, FCAS, passed away in November 2025, in Sparta, New Jersey. Flynn, who served as CAS President from 1993–1994, was born in Peckville, Pennsylvania, the middle sibling of six brothers and sisters. He and his family lived in Greenbelt, Maryland, before moving to San Francisco when he was 15. He graduated from St. Ignatius High School, received his B.S. in math from San Francisco State University. He worked in several firms, including Crum & Foster, where he was appointed chief actuary. Flynn was also a volunteer for the U.S. State Department. After the collapse of the Soviet Union, he traveled with other U.S. financial professionals to educate Eastern European officials on standard Western financial practices. Flynn settled in Sparta, New Jersey. Locally, Flynn volunteered as an assistant scoutmaster for the Boy Scouts and served as a deacon at the Sparta Presbyterian church. After retirement, Flynn volunteered as treasurer of People Help of Sussex County for many years and served as a member of the Sussex County Democratic Committee. Flynn was a proud father to five children: Michael, Colleen, Erik, Elizabeth, and Karen, who predeceased him. He was grandfather to seven and a great-grandfather to 11. In his spare time, Flynn enjoyed reading extensively, traveling the world, visiting family, or relaxing at their lakeside cabin in Maine with his beloved wife of 45 years, Sally Larson.

The Faithful, Traveling Mathematician

1957–2026

David Lee, FCAS, CPCU, passed away in January in Bloomington, Illinois. He graduated from Floyd Valley High School in 1976. He earned his B.A. in mathematics from Northwestern College and his M.S. in statistics from the University of Nebraska. He had a distinguished 35-year actuarial career at State Farm Insurance, finishing as Countrywide Pricing Director in the Property and Casualty Actuarial Department. Lee volunteered with the CAS from 1987–2011, most notably serving as the vice president of Admissions from 2008–2011, garnering him the Matthew Rodermund Memorial Service Award. Lee was a lifelong athlete, lettering in college baseball and football, and later playing on community baseball and softball teams. Lee also founded and coached a middle school travel baseball team (the Bullets), benefiting dozens of student athletes in the community. In his retirement, Lee often played golf at Ironwood Golf Course. Lee’s favorite way to end the day was sitting on an upside-down bucket, casting a fishing line into the neighborhood pond. A devout Christian, he leaves behind a legacy of dignity, steadfastness, faithfulness, kindness, and generosity. Lee’s family will miss traveling with him but will not lovingly miss his nonstop math quizzes. Lee is survived by his wife of 49 years, Cindy; three children, Susan (Dan) Nelson of Thompson’s Station, Tennessee; Tom (Sydney) Menning of Fox Lake, Illinois; Lea (Jim) Nelson of Bloomington, Illinois; seven grandchildren: Avery and Romey Nelson; Riley, Leighton, Margot, and Lucy Menning; and Evelyn Nelson; and two siblings, Bruce (Cathy) Menning and Kaye Bennett. Lee was preceded in death by his parents, Alden and Connie Menning.

In Memoriam

1940-2025

David Lee Menning (FCAS 1986)

1957-2026

membernews

Making Things Happen

Chandu Patel: Saying “Yes” and Showing Up

Chandu and Hima Patel enjoying Chiang Mai, Thailand.

handrakant (Chandu) C. Patel, FCAS, MAAA, is a name synonymous with dedication, leadership, and innovation in P&C actuarial practice. With more than three decades as both a practitioner and a volunteer leader, Patel has quietly shaped how actuaries understand and perform reserving — one of the most crucial and complex activities in insurance. His long‑standing service with the CAS has not only advanced the profession’s technical capabilities but has also fostered opportunities for others to grow in their careers and contribute meaningfully to actuarial research.

Patel’s journey with the CAS began shortly after he achieved Fellowship in 1994. Fueled by a desire to contribute back to the profession that had nurtured his own development, he raised his hand to grade and set exam questions — an early and essential form of service that impacts every new Fellow who follows. From there, he expanded his volunteer footprint into continuing education and research, joining the Casualty Loss Reserve Seminar (CLRS) Working Group and the Reserves Working Group. Over time, these early roles grew into significant leadership responsibilities that now influence the CAS’s research agenda and member development offerings.

Today, Patel serves as chair of the CAS Reserves Research Working Group, vice chair of the CLRS, and as a member of the CAS Discipline Committee. In these capacities, he performs a remarkable balancing act between guiding high‑impact research, planning large‑scale professional seminars, and upholding the integrity and accountability of the profession.

At the heart of Patel’s volunteer contributions is his leadership of the Reserves Working Group. Under his guidance, this group serves as a beacon for practical, innovative, and timely reserving research for the CAS membership. The working group’s mission is to identify pressing issues in reserving, sponsor research on those issues, and shepherd high‑quality work through to publication — all in ways that maximize relevance for working actuaries.

In recent years, the Reserves Research Working Group has produced an impressive body of research papers offering practical insights on applying emerging technologies and methodologies to reserving challenges. These papers help actuaries stay current with advances in data science, predictive methods, and real‑world practice needs. Many of these published studies are showcased at professional meetings such as the CLRS, ensuring that research findings translate directly into tools actuaries can apply in their daily work.

The group’s call paper programs have created an accessible pathway for analysts, academics, and seasoned practitioners alike to publish on topics of evolving importance. This structure not only expands the body of reserving literature, it nurtures new research talent — something that Patel deeply values as part of his volunteer mission.

Looking ahead, Patel and his colleagues are preparing an ambitious paid research proposal to develop an AI‑assisted reserving tool. The goal is to help reserving actuaries at every stage of the process, from selecting methodologies to conducting peer reviews and strengthening documentation. In addition, the working group is planning an exciting 2026 Call for Papers focused on evolving technology for data handling, manipulation, and application to new reserving methodologies.

For Patel, the goal of all this work is straightforward: to keep members abreast of the latest developments and provide them with tools that make them more successful in their jobs. His leadership reflects a belief that research should be both rigorous and practical, serving the profession as a whole.

Beyond research, Patel plays a key role in organizing one of the CAS’s most respected professional education events: the CLRS. As vice chair, he collaborates with fellow volunteers to brainstorm seminar topics, recruit expert speakers, and design an agenda that reflects the evolving needs of reserving actuaries.

CLRS consistently draws hundreds of professionals eager to deepen their technical skills and stay current with industry trends. Through his work, Patel helps ensure that the CLRS remains relevant, forward‑thinking, and deeply connected to the day‑to‑day practices of reserving actuaries.

Patel’s commitment to the actuarial profession extends beyond CAS volunteer roles. He has over 38 years of experience in P&C reserving and financial reporting, including senior actuarial roles with prominent insurers. This professional foundation gives him a deep perspective to draw from when guiding research initiatives or shaping seminar content.

Along the way, he has earned recognition for his contributions. Notably, in 1998 he received the CAS Reserves Prize for the best reserve paper, an early professional honor that foreshadowed his wider impact on the field. He has also contributed to the profession through editorial work, including involvement with a book on catastrophe management.

Reflecting on what he is most proud of, Patel points to the relationships he has built through volunteer service — especially the note of appreciation from a seasoned member who told him he was the best working group chair with whom he had worked. For Patel, that recognition meant more than awards; it affirmed that how a volunteer leads matters just as much as what gets accomplished.

Throughout his volunteer journey, Patel has been motivated by a desire to give back. “The CAS has provided me with a tremendous opportunity to educate myself and to further my career more than I had ever hoped,” he reflects. “I volunteer to give back and to provide the same opportunities to others.”

Patel’s volunteer journey is a masterclass in service, leadership, and generosity of spirit. From exam grading rooms to research committees, from seminar-planning sessions to discipline oversight panels, he has given his time and expertise to make the CAS stronger, more innovative, and better prepared for the future.

Patel’s dedication to his craft is matched by his love for life beyond work. He and his wife share a passion for travel and adventure, recently exploring Vietnam and Thailand.

As the CAS continues to evolve in an era of emerging technology, data transformation, and shifting industry dynamics, volunteers like Patel provide the steady anchor of experience, vision, and commitment that the profession needs.

His story is an inspiring reminder that making things happen often starts with saying “yes” and showing up for the community we serve.

CAS Staff Spotlight

Meet Max Baskin, CAS Data Analyst

Max Baskin

elcome to the CAS Staff Spotlight, a column featuring members of the CAS staff. For this spotlight, we are proud to introduce you to Max Baskin.

- What do you do at the CAS? How does your role support the Strategic Plan?

I began my role as a data analyst in October 2025. My primary role this year is to support the transition to our new association management system and help ensure that the CAS candidate and member online experience is as smooth as possible. This involves supporting exam score releases, fixing data and system errors, liaising with our IT development partners, and more. I also help empower other CAS staff by creating dashboards, helping to set up mass emails, and providing general IT and data analysis support. This all allows me to help support the CAS Strategic Plan, especially regarding enhancing the candidate experience and advancing operational excellence.

- What inspires you in your job and what do you love most about it?

Data analysis is not just a science; it is an art. At first glance, the work of data science and visualization might seem straightforward, but I’ve found that there are actually a lot of really interesting nuances regarding design choices, audiences, and emphasis. Whenever I work together with the IT team to create a complex Excel table or dashboard for our stakeholders, I always enjoy considering how others will view our products from their own perspectives and thinking about what I can do on my end to make the data even more beautiful.

- Describe your educational and professional background. What do you bring to the organization?

Before graduating last year, I had internships in various fields, including IT support, victim/witness assistance, fraud analytics, and more. While all of these experiences were in different industries, they all involved data analysis and IT to at least some extent. This, combined with my academic background in statistics, has helped me contribute to the operations and long-term goals of the CAS.

- What is your favorite hobby outside of work?

I play guitar and love to bike on Northern Virginia’s outdoor trails. My goal this year is to bike the entire length of the Washington and Old Dominion Trail, from Alexandria to Purcellville (almost 45 miles).

- If you could visit any place in the world, where would you go and why?

When I get the chance, I’d really like to visit Greece, especially Crete. The history of the country has always fascinated me, and the food is a plus too!

- What would your colleagues find surprising about you?

In college, I volunteered for an anonymous student-run mental health support and referral hotline. I never studied psychology or social work formally, but the training I received and experience I gained from my two years with the line have really helped me understand the topic more thoroughly.

- How would your friends and family describe you?

People know me as someone to come to if you need a tidbit of knowledge or trivia about absolutely any topic, from history to literature to science. I read a lot, and it really helps me clean up at quiz bowl and trivia nights!

2025 Annual Report of the CAS Discipline Committee Released

he CAS Rules of Procedure for Disciplinary Actions (as amended May 3, 2009, by the CAS Board of Directors) requires an annual report by the Discipline Committee to the board of directors and to the membership. This report shall include a description of its activities, including commentary on the types of cases pending, resolved, and dismissed. The annual report is subject to the confidentiality requirements.

The CAS Discipline Committee received a complaint in February 2025 alleging possible material violations of Rules 1 and 2 of the Code of Professional Ethics for Candidates by a CAS actuarial candidate. An investigation panel was convened; its report was issued at the end of August 2025 and recommended discipline. In accordance with the CAS Rules of Procedure for Disciplinary Actions involving Candidates, a Discipline Committee Panel was convened and held a hearing in November 2025 to review the recommendation and record provided by the investigation panel and to render a decision on discipline.

The Discipline Committee Panel unanimously concluded that the subject candidate materially violated Rules 1, 2, and 7 of the CAS Code of Professional Ethics for Candidates and concluded that a significant restriction on the subject candidate’s CAS exam eligibility was warranted. The Panel therefore ordered that the subject candidate be barred from taking future CAS examinations and that the subject candidate may be allowed to take future CAS examinations only upon their request to, and approval by, the CAS Discipline Committee.

This decision is final and binding as the subject candidate did not appeal the decision.

There were no cases pending before the committee as of the date of this report.

January 19, 2026

CAS Discipline Committee Panel Issues Ruling

he Discipline Committee Panel of the Casualty Actuarial Society (CAS), acting in accordance with the CAS Bylaws and the CAS Rules of Procedure for Disciplinary Actions Involving Candidates, and with consideration of the findings and recommendation from the CAS Investigation Panel, voted unanimously to bar Amy Tau from taking future CAS examinations for materially violating Rules 1, 2, and 7 of the Code of Professional Ethics for Candidates (the “Candidate Code” or “Code”).

The Panel found that Ms. Tau materially violated Rules 1 and 2 by misrepresenting that she sat for a CAS examination, knowingly submitted false time entries to her then employer to make it appear as if she was sitting for a CAS examination when she was not, and altering a prior CAS grade report that she then provided to her employer. Additionally, Tau failed to respond to the investigation inquiries and did not respond or appear for the Discipline Committee Panel hearing, materially violating Rule 7 of the Candidate Code.

Tau may be allowed to take future CAS examinations only upon her request to, and approval by, the CAS Discipline Committee.

The appeal period has expired without appeal, and the Panel’s decision is final.

Celebrating the 2025 CAS Volunteer Award Winners

ach year, thousands of CAS volunteers contribute their time, expertise, and energy in ways that strengthen our profession and support members at every stage of their careers. The 2025 Volunteer Award recipients represent the many paths through which volunteers make a difference — from education and research to engagement, leadership, and community building. As National Volunteer Week approaches, running from April 19 to April 25 this year, it’s the perfect time to spotlight these inspiring volunteers.

What follows are reflections shared directly by many of this year’s honorees, along with profiles highlighting the service and impact of others, all of which showcase the passion, commitment, and collaborative spirit that define CAS volunteerism.

New Member Award

Don’t be afraid to ‘shop around’

Jessica Ackley, ACAS 2022

“I always say that I volunteer for the CAS because so many of the people closest to me are actuaries, and I want to provide the varied perspectives of everyone I know and do what I can to help improve things. My husband is an FSA, my younger brother recently earned his ASA, two of my very best friends are an FSA and an FCAS, and I still see many of my college friends (actuarial science majors) regularly. I joke that I can’t seem to get away from actuaries. I joined a small triathlon club a few years ago and, after a few workouts, found out that one of the women was an FSA.

Ackley

“I really enjoyed writing an article in Future Fellows last spring that covered details on how the PCPA transition deadline would work. Based on the conversations we were having while I wrote the article and questions that I raised, the deadline changed to January 1, 2026, and we were able to make the transition timeline a bit smoother for candidates. I felt like the article was a really helpful resource for candidates and employers as they navigated the change.

“Don’t be afraid to ‘shop around’ a bit regarding volunteering; all of the CAS groups I’ve volunteered with have a different structure and feel to them. If you join a group and don’t feel like it’s a good fit for whatever reason, try a different group when the next volunteer survey rolls around.

“Since I’m in the Candidate Advocate Working Group, please tell the candidates you know to keep an eye out for the Candidate Survey coming out later in 2026. The survey results are intended to directly influence the priorities of our group and other groups in the CAS.”

Just jump in

Josh Meyers, FCAS 2023

“What I enjoy most about volunteering is the chance to connect with people throughout our profession. Working on the CAS AI Fast Track gave me the opportunity to talk to actuaries from all over who are helping push the profession forward. When I worked with an exam committee, I spent several months with the same group, and it was great to build relationships with people I never would have crossed paths with otherwise. Getting to meet and learn from so many different people has been the most rewarding part of volunteering for me.

Meyers

“I’m going to pass along the same advice I saw in the Actuarial Review a few years ago: Just jump in. There are so many ways to volunteer with the CAS, and you do not need to have it all figured out at the start. There are also plenty of opportunities to start small with just an hour or two each week. Try a few different things and see what works best for you.

“Do not be afraid to reach out and talk to the CAS staff. I have worked with staff across the organization, including people who design exams, organize events, and support continuing education, and every one of them has been friendly and great to work with. Even if there are no volunteer opportunities listed, reach out and ask what is in the works. They are always happy to help you get connected.”

Find your passion and give it your best

“Volunteering for the CAS has been a great learning experience, whether by doing my own research to write various articles or from discussions with other CAS volunteers who are quite accomplished, and I consider them thought leaders in the field. Writing is also a skill I’ve been meaning to cultivate, so volunteering with the CAS has given me the opportunity to develop this skill and get feedback from professionals to help my career growth.

Nawar

“When I started volunteering with the CAS, I was impressed by how motivated, engaged, and dedicated everyone is. While brainstorming with Jim Weiss on the thesis of one of my papers, we spent over an hour slicing and dicing all the arguments until we were able to come up with a great conclusion. I got very motivated having this discussion, especially with someone as brilliant as Jim. When my colleagues and friends come to me asking questions about my ideas, it’s quite rewarding.

“Find a working group whose mandate is something you’re passionate about and then give it your best. It’s a very rewarding experience and I’m lucky to be part of the Actuarial Review Writing Subgroup.”

Rehan has been a driving force in expanding the CAS’s influence and leadership on the global stage. Through his work as vice chair of the International Actuarial Association Climate & Sustainability committee and as an active member of the CAS Climate and Sustainability Working Group, he has helped raise the Society’s profile on climate and sustainability topics among international peers.

Siddique

Above and Beyond Achievement Award

Passion is contagious

Louis-Philippe Caron, FCAS

“As a person and an insurance professional, I always believed in the importance of personal and professional growth, networking, and giving back to the community and the industry that has shaped my career. Serving not only allows you to volunteer your expertise and time to support an organization but also benefits you personally and professionally. It is a transformative opportunity to build your skills in new areas, work on projects you ordinarily do not have the chance to, and build new connections with professionals in your industry and beyond. Building on my passion for advocating and contributing to my community and our profession is and has been an ongoing source of fulfillment and happiness for me.

Caron

“What stands out to me is how passionate and determined the great majority of volunteers are. That passion is contagious and helps the teams deliver better outcomes together; the group is always better than the sum of the individuals.

“As a co-lead of the Future of Volunteerism Task Force, I strongly advocated for the shift to a more balanced staff and volunteer model with better defined accountabilities and objectives. I am very happy with the recent evolution of the CAS and am convinced that we have put in place the right model to accelerate our growth and ensure a better future for all stakeholders.

“You are never too young or inexperienced to start your giving back journey. Go at your own pace, given the time that you have; small is beautiful. Micro-volunteering is a great way to get your feet wet and to start your CAS volunteering journey.

“Get involved. You will never regret it. It will be rewarding on both a personal and professional level.”

“I volunteer for the CAS because I care deeply about the profession and the people in it. The CAS played a huge role in my own development, and volunteering is my way of giving back while helping shape what comes next. I’m energized by collaborating with passionate volunteers and staff to create meaningful education, promote professionalism, and build a community that supports actuaries at every stage of their careers.

Huenefeldt

“Incidentally, many of my favorite volunteering memories involve karaoke, which may or may not say something about me! From belting out songs in Vegas with fellow facilitators after the Course on Professionalism, to karaoke nights at the CAS Leadership Summit with volunteers and staff, to heading out with friends after speaking at CLRS or the Annual Meeting — those moments always rise to the top. They’re a reminder that while the work we do for the CAS is important, the friendships, laughter, and occasional off-key singing along the way are what make volunteering truly unforgettable. (And in case anyone was wondering, my go-to karaoke song is ‘Total Eclipse of the Heart’ by Bonnie Tyler.)

“What I’m most proud of in my volunteering is helping move meaningful professionalism initiatives from idea to execution. During my leadership roles with the Professional Education Working Group, I had the opportunity to help expand the Course on Professionalism to better reflect the skills actuaries need in practice, most notably incorporating communication skills in 2019.

In 2020, when the pandemic disrupted in-person courses, we quickly pivoted to create a virtual option so candidates could continue progressing toward their credentials without interruption. More recently, when bias topics were added as a requirement to the U.S. Qualification Standards, we developed content to ensure candidates could meaningfully fulfill that requirement. Together, these efforts helped keep professionalism education relevant, accessible, and aligned with the evolving expectations of the profession.”

Collaborating benefits the CAS and my job

Jamie Mills, FCAS

“The actuarial career has given me so many opportunities to grow, learn, and do meaningful work. Volunteering is my way of giving back, to help create similar opportunities for others entering or advancing within the profession.

Mills

“For each of the committees I’ve had the privilege of leading, I have always been impressed with the engagement and drive of the committee members. It’s inspiring to witness the engagement and passion of the volunteers, and it emphasizes what all we can accomplish when we bring a great group of actuaries together with a common goal.

“I’m incredibly proud of how engaged and collaborative our Ratemaking, Product and Modeling Seminar Working Group is. Everyone is genuinely committed to putting on a world-class seminar, and the teamwork makes the process both productive and enjoyable. The relationships we’ve built along the way are a big part of what makes the experience so rewarding.

“My recommendation to new members is to find something that interests them and that they are passionate about. Being engaged from the start will serve you and the CAS well and will help you on your volunteering journey.”

Creating a meaningful forum

Terence “Terry” Richard Robinson, ACAS

Posthumous Award Recipient Terence (Terry) Richard Robinson was a dedicated CAS volunteer, respected colleague, and deeply engaged member of the actuarial community whose impact continues to be felt across the Society. Terry passed away unexpectedly in December 2024. He served as chair of the Reinsurance Working Group within the Research Council.

Terry began volunteering shortly after earning his ACAS in 2013. He had remained actively engaged until just days before his passing. Over more than a decade of service, he held numerous leadership and volunteer roles, including four years as chair of the Reinsurance Working Group and service as a University Liaison with Temple University, where he earned his actuarial science degree. As chair of the Reinsurance Working Group, he was passionate about ensuring the working group served as a meaningful forum for strengthening actuarial knowledge and advancing reinsurance research.

Known for his intellectual curiosity and generosity with his time, Terry was a steady and enthusiastic contributor to CAS research initiatives. Even in his final days, he remained focused on supporting a research project, reflecting his deep commitment to the profession and the Society. He also had an active presence on LinkedIn, where he shared insights with a wide professional audience and helped extend CAS conversations.

Professionally, Terry was an assistant vice president at Old Republic Specialty Insurance Underwriters and previously worked at JLT Towers Re, Guy Carpenter, and Towers Watson. Beyond his actuarial work, he was a person of eclectic interests and talents — an Eagle Scout, writer, photographer, performer, and co-host of “Mage: The Podcast.” He lived by a principle he often quoted after acts of generosity: “A Scout is helpful.”

Terry is remembered for his warmth, curiosity, and ability to connect people across disciplines. This award honors his lasting contributions to the CAS and the generous spirit with which he served the actuarial community.

Becoming a better actuary

Jaris Wicklund, FCAS

“I’m very proud of being a member of the CAS, and I want to help ensure it becomes the best organization that it can be. The vast majority of my volunteering to-date has been in the area of university engagement. The future of the CAS is dependent on finding, attracting, and educating the next generation of members, and I have always been passionate about being involved in these efforts.

Wicklund

“I think the thing I am most proud of from my time volunteering so far is helping craft the initial CAS Student Central Summer Program. In 2020, a large number of students had internships canceled, and a small group of us were challenged to create something to fill that gap. I think we built a truly meaningful and valuable experience for those students in a very short time, and I’m really proud of how we all pulled together to make it happen. That program has become a pillar of the CAS’s offerings to university students, and I am proud to have had a hand in creating it.

“Lean into what you are passionate about. There are a wide variety of volunteer opportunities from research to engagement to exam writing to finance and investments. Anything you are interested in, I am certain there is a volunteer opportunity for you. Please feel free to reach out. I would love to connect and learn more about what you are passionate about!”

Strengthening CAS ties with Asia

Janet Yang, FCAS

Janet Yang has long been a dedicated volunteer for the CAS and a passionate advocate for the actuarial community in Asia. Her service began with significant contributions to the CAS Exam Committee in Canada and has continued with sustained impact since relocating to Hong Kong. Yang has worked tirelessly to strengthen CAS’s visibility and engagement in the region, fostering collaboration across local actuarial organizations and serving as a key liaison for CAS activities.

Through her involvement with Asia Region Casualty Actuaries (ARECA), she helped restructure the ARECA Scholarship and secure sponsorship for its inaugural case competition — initiatives that have meaningfully advanced student engagement. She regularly leads CAS information sessions at universities in Hong Kong and contributes to professional education programs across the region.

Building on this extensive volunteer experience, Janet Yang has recently taken on the role of president of ARECA, where she will continue to expand member engagement, facilitate conferences and university outreach, and deepen connections with actuarial partners across more than a dozen markets.

Matthew Rodermund Memorial Service Award

Challenge the status quo

Sean McDermott, FCAS

“Years ago, I would have replied with the typical ‘to give back’ answer. Now, many years later, I volunteer to stay connected, maintain old friendships, meet new people, and stay relevant.

McDermott

“Over the years, I have watched the CAS team grow, and I have many fond memories and valuable CAS staff friendships.

“I was on the Executive Council during the CAS/SOA merger discussions and in the room for the final decision. This was an interesting time to be part of the CAS leadership, and the memories of the meetings/discussions will always be a highlight.

“I am proud of the support of my family during my years as a CAS volunteer. During certain times, the CAS volunteer commitment required additional travel that was added to an already busy work life and travel schedule. We made it work! The advice is simple. Just start!

“Pick a committee that interests you and look for ways to improve the committee’s process and create valuable changes to the tasks at hand. Do not be afraid to challenge your committee’s status quo or long-term embedded processes. You are on your committee to lead and make intelligent changes. Change is good!”

Lifelong friendships are invaluable gifts

Jim Merz, FCAS

“I feel that I have gained so much from being a member of the CAS that it is my obligation to give back to the community. It is fulfilling to feel a sense of accomplishment when working with other like-minded professionals for the good of the Society.

Merz

“One of my fondest CAS memories is the celebration dinners when I first joined a grading committee. There was a sense of accomplishment and joy to have worked hard to get the exams graded and pass marks set.

“I am most proud of the variety of types of volunteering and the length of continued service. Try volunteering because you might find that you like it!”

On behalf of the entire CAS family, we are grateful to all our volunteers who make a difference each year!

Printing Property: The Risk and Opportunity in a 3D Printed World

he year is 2025, at a time when the majority of us haven’t been on a 3D printing construction site. How would a building be 3D printed? How does 3D printing work?

I want you to visualize the process of soft serve ice cream at a fast-food restaurant. The premixed ice cream is dispensed from a metallic head at a constant speed, while the server skillfully maneuvers his hand, circling the cone while lowering the position as the ice cream builds on top.

This analogy is in essence how 3D printing works: a malleable substance being dispensed layer by layer into specific shapes. In the ice cream example, the shape is a cone, and in the 3D printing building example, it is (usually) a vertical wall slab. One fundamental difference between making soft serve and printing a building lies in the relative locations of the dispenser and the nozzle. For the soft serve, the nozzle — the metallic head where the substance is dispensed — stays static, while the receiving cone makes the movement, calibrated to achieve the desired diameter, height, and shape. For the large-scale 3D printed building, the site stays static while a giant nozzle controlled by a 3D axis system conducts the movement, drawing a smooth line with premixed concrete, tracing along a predetermined path that over time, in a sedimentary manner, will become a monolithic mass.

Background

With the same 3D print job file, you can print from anywhere and from any machine, as long as it’s professionally calibrated with any kind of printing materials, ranging from corn-derived polylactic acid to highly engineered concrete, and at any scale, from a desktop miniature to a civic building block. The loss in translation of the geometry is minimal due to the coded pathway that dictates how it prints. With a 3D printer, you are free from the limit of having the expertise onsite, with no fear of miscommunication across teams or loss of information in the transition and translation between platforms.

Overall, the scalability, duplicability, and humanless features make 3D printing extremely appealing to both investors and innovators around the world. Venture capitalists from San Francisco are funding start-ups in Texas (and other places in the U.S.2), while higher education institutions in the Netherlands3 and Switzerland4 are releasing groundbreaking innovations that make the technology more powerful every day.

As investors and innovators are making plans for expanding the endeavor, the insurance world has been relatively quiet on the subject. The aim of this article is to unpack this technology and initiate a discussion of the opportunities and risks of 3D printing as a construction method, especially as it impacts the property insurance market.

Buildings and insurance

While it was not discussed during the session, I wondered if this lack of synergy and urgency comes from the segregation among experts from different industries.

The evidence displayed at an actuarial conference for some building materials being safer than others is clear and sound. However, when it comes to choosing building materials, insurers don’t have much leverage to make the builder choose the construction materials. The risk profile of a building is determined by the design (the architect), the construction (the contractors), and the price (the suppliers). By the time the underwriter or the actuary is involved in the project, it’s too late. It usually isn’t until the house is near completion that the homeowners start to shop for insurance policies. Homeowners are also learning too late that they could have made different decisions that would have affected their coverages and prices.

When the major insurers in California withdrew from the homeowners market, it was largely due to the uninsurability of the houses in the wildfire-prone areas.6 Among the corporate evacuees, we see a strong trend among decisions made from 2021 and onward. Many major firms stopped issuing new policies, and some stopped renewals of property coverages in California. Many quoted the reasons being the increase in cost of construction and inflation.6

If the houses being built are too expensive to repair and replace, the conflict between insurance and construction boils down to the conflict between insurability and housing shortage. Both sides are doing what they have to do: insurers exit the market because it need to stay solvent; homeowners build in undeveloped wildfire-prone land because they run out of places to build.

When 3D printing enters the room

While investors and innovators are celebrating the cost efficiency and high fidelity of 3D printing buildings, insurers and regulators may find themselves advocating for this particular fabrication method for their own reason — risk reduction.

3D printing material for buildings is primarily concrete with reinforced rebars. Much like traditional concrete buildings, the material has similar fire resistance performance and isn’t easily destroyed by heat or smoke.7 A commercially available 3D exterior wall is claimed to have “a fire resistance rating of more than 2.5 hours per ASTM E119 and interior walls have a fire resistance rating of 117 minutes.”8

Apart from the reduced property damage side of the advantages, a 3D printed building may also eliminate certain liability risks during the construction process. Due to the minimal number of human workers on site, the insurance exposure is foreseeably reduced. The type of work is also much less risky than traditional construction, since humans are eliminated from tasks involving heights, heavy weights, or falling items. The most common task is to monitor the printing process, and the most likely injury risk is probably reduced to sunburn. Jokes aside, the cost of savings in workers’ compensation for developers and investors can be a significant incentive for the adoption of 3D printed buildings.

Another aspect, which is not directly linked to risks but should add more credibility to this construction method, is that it can be used for building. Since a printer can operate autonomously in conditions with unfavorable temperatures and no oxygen, governments and large tech companies are investing in experiments and projects to send printers to the moon to accomplish a task that is impossible for human astronauts to do.

The dark side of the moon

Because it’s printed from a refined nozzle and geometries are calibrated and optimized, a 3D printed wall will use significantly less concrete, making it more affordable and easier to construct than traditional concrete buildings. However, the reduced thickness increases the risk of brittleness, especially in terms of wind or earthquake resistance, but the actual impact will require more refined research.

Resistance against lateral force is another concern. Typically, current 3D printing technology fabricates in a sedimentary manner, producing layer after layer of material on a horizontal plane. To visualize this, recall the earlier soft serve ice cream analogy. What happens if your soft serve is built too high? It falls over, and you have less ice cream to enjoy. With sedimentary layers, tolerance of lateral force is weak. A 3D printed concrete wall is not as strong as a conventional concrete one, which has reinforced rebar that goes in both horizontal and vertical directions. To overcome such a shortfall, a comprehensive structural system is needed. Because of this weakness, existing 3D printing projects generally don’t exceed two floors because they lack reinforced vertical stability.

Risks aside, the technology itself has some hard thresholds to overcome. The 3D printing process is not strictly human less in any practical sense. The initial file creation requires an extremely high level of expertise. Knowledge about 3D modeling and the building’s construction are essential. Adding industrial experts to the staff of architects and designers will add costs to the project. Additionally, the starting stage of the actual printing process demands rigorous calibration, a process that takes in depth knowledge of the machine, as well as experience in troubleshooting. Most printing job failures occur at the beginning: rough or uneven platforms can jeopardize the rest of the print.

Once the file is created and the machine is calibrated, the rest of the process doesn’t involve a human’s touch. The general practice on a 3D printing site usually requires one engineer to “supervise” — that is, watch the printer in case anything abnormal happens: nozzle blockage, irregular extrusion of material, missing layer (due to nozzle blockage), etc. Such supervision is instrumental, especially for an open-air printing job (i.e., not in a controlled environment), and a mistake is consequential — it usually means hours of work and printed material is wasted, and if not caught early, the job may need to be restarted.

Speculation

Companies like ICON and Vertico are generating useful data and rapidly expanding the applications of 3D printing construction. Such total digitalization will change the landscape of data collection and analysis. We will have more accurate exposures, more timely reports on damage and cost, and more precise correlations between exposure and loss. It’s not science fiction that in a few years many of our constructions can be 3D printed, whether it’s motivated by cost saving, fireproofing, or the intricacies of construction. It’s our responsibility as risk professionals to understand what is coming toward us.

At a time when professionals are highly specialized in their own field, it’s unconventional and challenging to look at problems from other industries. I’ve seen amazing research done in vertical fashion, but it’s also important to look at problems horizontally. As insurance professionals, being curious about tangential knowledge that’s traditionally outside of our expertise will empower us to advocate for choices that serve us better collectively and will generate more synergy across boards. Collaboration and communication are the keys to open up solutions and new horizons for our field.

References

- History of 3D printing: It’s older than you think

- ICON, a pioneer in the 3D printing of homes, raises $56M led by Norwest, Tiger Global

- Vertico News

- Mechanics and Materials Laboratory — 3D Printing

- Wildfire Prepared: Practical, Proven Steps to Safeguard Homes and Communities, Alister Watt, CAS Annual Meeting, Austin, TX

- References:

- Fire performance of innovative 3D printed concrete composite wall panels — A Numerical Study, Thadshajini, Perampalam Gatheeshgar, Irindu Upasiri, etc.

- ICON Wall performance

- ICON Build — Story

Surface Tension

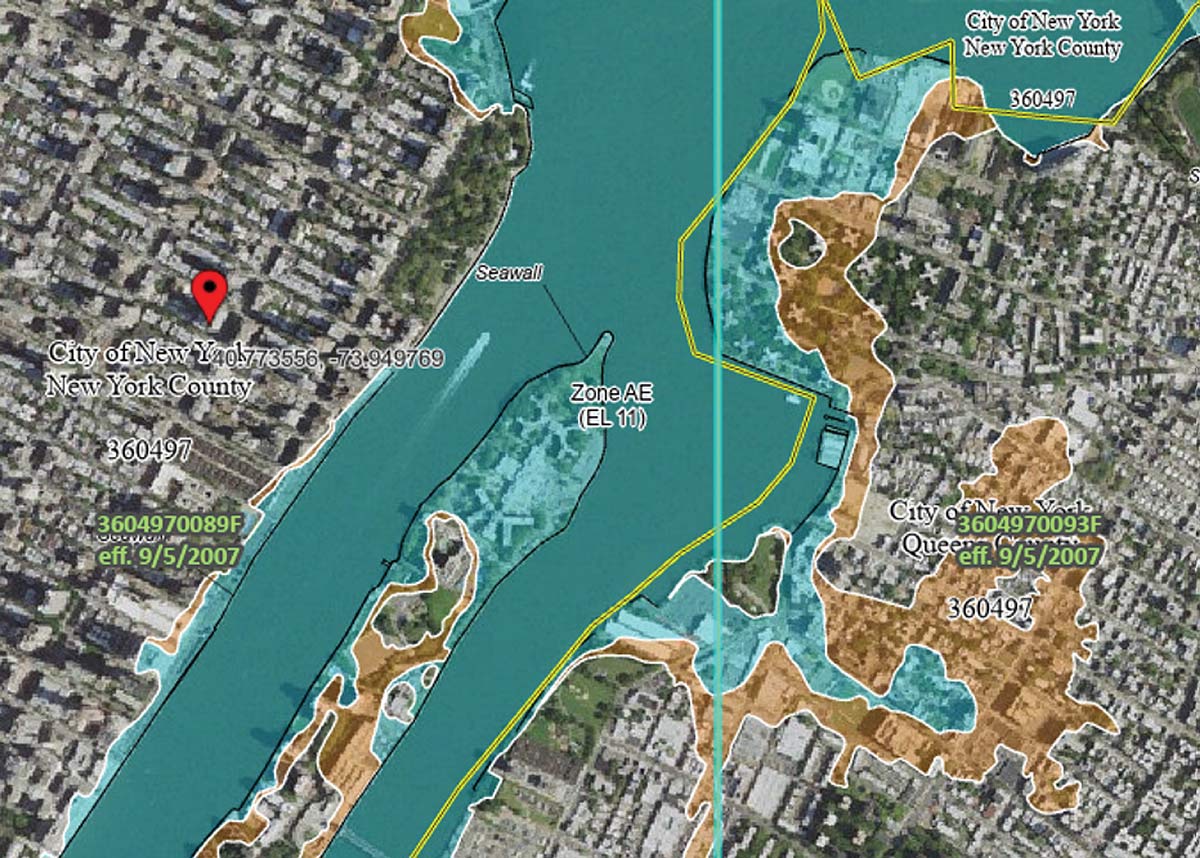

loods rarely arrive the same way twice. Some are driven by hurricane-induced storm surge that pushes seawater inland block by block. Hurricane Harvey behaved differently, hovering over the Gulf Coast for days and dropping feet of rain on Houston. Sometimes a river slowly exceeds its banks after days of steady upstream rain, and sometimes it rises with extraordinary speed after heavy localized rain, as was seen in the tragic Kerr County, Texas, event in 2025. And increasingly, it’s none of those things; instead, we’ve seen intense cloudbursts overwhelm streets, basements, and storm drains in places that don’t think of themselves “flood-prone” at all.

Insurance coverage has failed to keep pace with this growing risk. Most households affected by inland or urban flooding still have no flood insurance at all, even after experiencing losses firsthand. This coverage gap is no longer a mystery of modeling. Flood risk today is better measured, more granular, and more legible than at any point in the past; both public and private actors can estimate property-level exposure with a degree of confidence that would have been unthinkable a generation ago, and modeling breakthroughs continue to accelerate. And yet uptake remains stubbornly low, especially outside the narrow slice of properties where coverage is mandatory.

That tension — between rising, increasingly visible flood risk and persistently limited insurance coverage — is the starting point for this article. Private flood insurance has finally become viable, supported by new models, new capital, and new regulatory pathways that barely existed a decade ago. But viability is not the same as reach. Without changes to how flood insurance is distributed, incentivized, and embedded into household decision-making, private flood will remain a niche solution: well designed and technically impressive, but still absent when people need it the most.

“Flood” is not just one peril

Coastal storm surge is the version of flood risk most people picture most readily. It is driven by wind pressure pushing seawater inland. Losses tend to track familiar geographies: barrier islands and low-lying coastal plains. The footprint can be large, but the risk is legible — people know they live “near the water.”

Fluvial (riverine) flooding is less intuitive because it is a system problem. A property can flood because of rainfall miles away, hours or days earlier, interacting with soil saturation, upstream development, and watershed geometry. River floods also span a spectrum: some are slow and forecastable, while others behave like flash floods when intense rain falls over a narrow area and channels fill faster than warnings can travel, trapping communities.

These differences make flood risk patchy and, in many places, invisible. Public understanding and many institutional triggers still anchor on binary categories, like being inside or outside of a Special Flood Hazard Area (SFHA), defined as having a greater than 1% annual chance of flooding. But much of today’s damaging flood experience does not respect those boundaries. The consequence is a persistent mismatch: households and mortgage lenders often treat flood as a niche coastal or river-adjacent concern, while losses increasingly reflect a wider set of mechanisms and geographies. That disconnect helps explain why flood insurance institutions have struggled to adapt.

How flood became a federal problem

This retreat coincided with a shift in how flood losses were handled politically. Large floods increasingly triggered federal disaster aid, infrastructure spending, and emergency relief. That response helped communities recover, but it also weakened the case for voluntary insurance. Flood risk, in practice, became socialized ex post rather than pooled ex ante, and this continues to be the case today.

The modern framework took shape in 1968 with the creation of the National Flood Insurance Program (NFIP). The NFIP was not designed simply to replace private insurance. It was built around a dual mandate that remains central to its identity. First, it aimed to make flood insurance broadly available in places where private markets would not operate. Second, it sought to reduce future flood losses by tying insurance availability to community floodplain mapping, land-use controls, and mitigation standards adopted by local governments.

The program’s delivery mechanism reflected this hybrid role. Under the “Write-Your-Own” (WYO) structure, private insurers sell and service NFIP policies under their own brands, while the federal government retains the underwriting risk and sets rates and terms. The arrangement leveraged private distribution and claims infrastructure without requiring insurers to put capital at risk. That structure has long created incentive frictions: flood is an administrative line rather than a strategic one, offering limited upside for insurers or agents, little reward for risk reduction, and few reasons to actively promote coverage outside mandatory purchase scenarios.

From the outset, the NFIP was asked to balance competing goals that would be difficult for any institution to reconcile. It was expected to be financially sound, politically palatable, widely available, and supportive of long-term risk reduction — all while operating in places where flood risk was highest and mitigation most expensive. That tension has shaped the program ever since, and it continues to influence how flood insurance is perceived today.

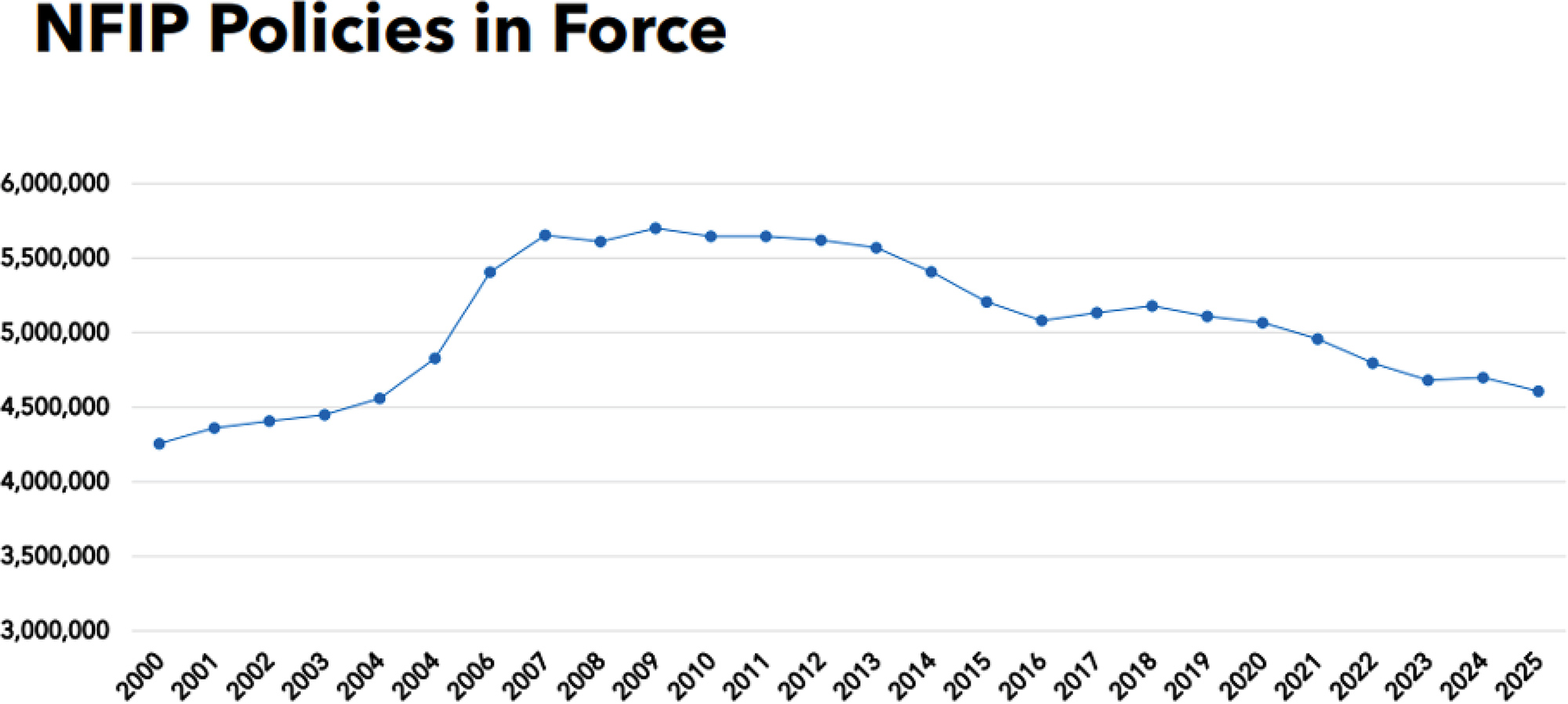

The NFIP today

The most visible expression of that shift is Risk Rating 2.0, FEMA’s overhaul of how flood risk is priced. Rather than relying primarily on broad flood zones and elevation thresholds, the updated framework incorporates multiple catastrophe models, property-level characteristics, and a wider set of flood risk drivers. The result is a rating system that produces far more differentiated premiums and aligns more closely with expected loss than its predecessors ever could.

Importantly, the NFIP’s modernization did not rely on a single model or vendor. The NFIP now blends multiple model views, empirical loss data, and portfolio considerations in ways that resemble best practices in the private market. Evans notes that while the NFIP has guardrails, “within the constraints it has it is now a pretty sophisticated pricing approach.”

Those constraints, however, remain substantial. Rates are subject to statutory caps and glide paths that limit how quickly premiums can adjust, even when updated risk signals point sharply upward. Coverage limits of $250,000 for residential and $500,000 for commercial are increasingly inadequate relative to replacement costs in many markets. In addition, the requirement for mandatory purchase of flood insurance is still tied to SFHAs, anchoring participation to legacy flood maps even as a growing share of losses occurs outside those zones. The result is a program that can assess risk with increasing clarity but cannot fully act on that information.

Private flood reemerges

Computing power eventually caught up. Katz describes how, by the early 2010s, “computers were finally getting fast enough that you could start to do this nationally and give carriers confidence in the results.” At the same time, data inputs improved dramatically. High-resolution elevation data, land-use and land-cover datasets, and better precipitation modeling allowed modelers to approximate surface runoff, ponding, and drainage behavior in ways that had previously been infeasible.

Those improvements mattered most outside traditional floodplains. In many areas classified as low risk under FEMA’s mapping regime, pluvial flooding dominated loss experience. Cities like Atlanta — where Katz notes there is no major river running through the city — were systematically underestimated, despite topography and development patterns that funnel water into vulnerable areas.

Equally important was the ability to translate model output into underwriting signals insurers could actually use. As Katz puts it, the breakthrough was not just better hazard science, but the ability to run models consistently, compare results across vendors, and integrate them into rating and underwriting workflows. Once that became possible, flood stopped being an unquantifiable tail risk and became something insurers could segment, price, and manage.

Regulatory changes removed the next barrier. When private flood policies were allowed to satisfy mandatory purchase requirements for federally backed mortgages, the market shifted from theoretical to viable. Without that recognition, private flood could only function as an excess or voluntary product. With it, insurers could compete directly for primary coverage, particularly for properties where NFIP pricing or coverage limits no longer aligned with perceived risk.

Capital followed these capabilities. As modeling improved, reinsurers grew more comfortable deploying capacity to flood programs — often with close scrutiny of accumulation management and underwriting discipline. A new ecosystem of MGAs, specialty carriers, and reinsurance-backed programs was thus able to grow.

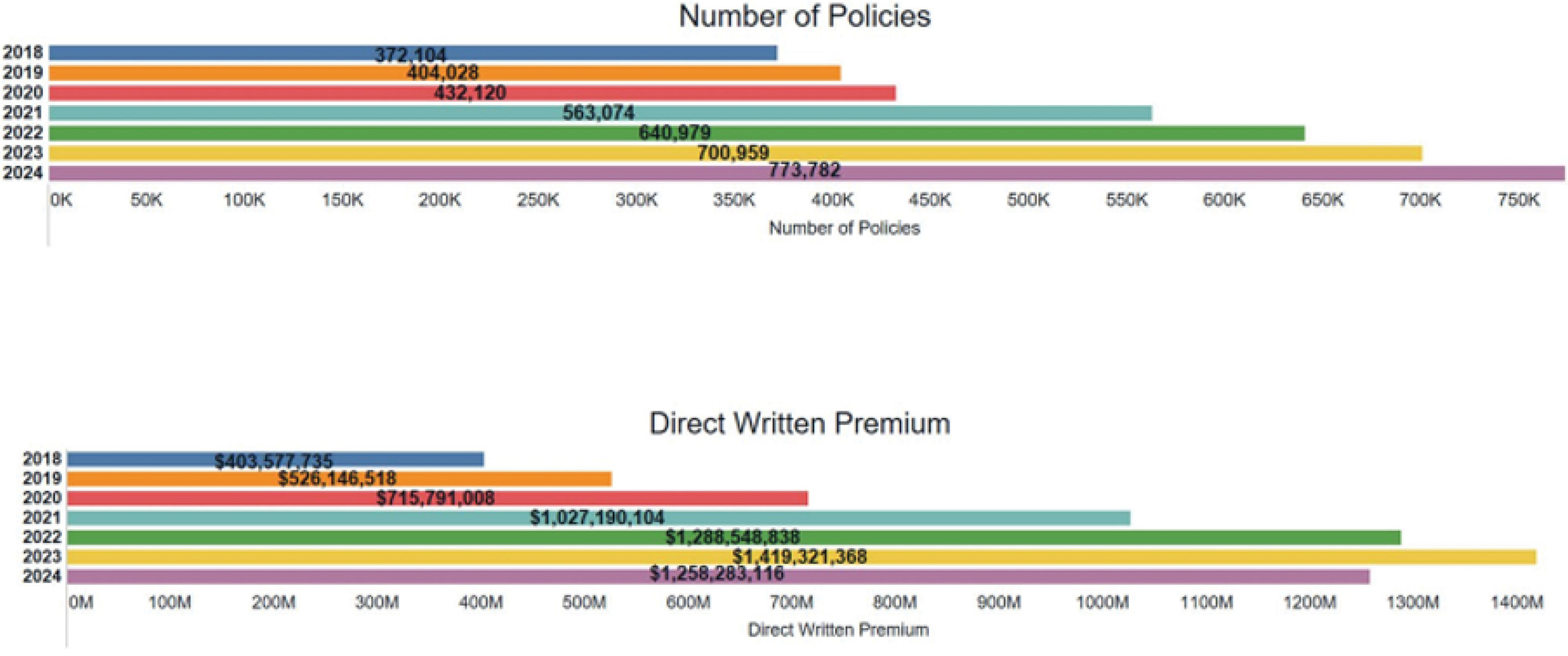

The private flood market that has emerged over the past decade is no longer hypothetical. A recognizable set of players and business models now demonstrates that flood insurance can be written, priced, and supported at scale. What the market has not yet demonstrated is how to translate that technical viability into broad adoption.

At the center of the market are specialist MGAs that have made flood their primary focus. Neptune Flood is the most prominent example, having built a national primary flood product that competes directly with the NFIP in many regions. Neptune’s growth — and its headline-grabbing 2025 IPO — validated the basic proposition that private flood could operate beyond narrow excess layers.

Reinsurers, meanwhile, have moved beyond passive capital provision. Firms like Swiss Re have developed increasingly integrated flood solutions for primary carriers and MGAs, combining modeling, pricing support, accumulation management, and quota share capacity. But as Evans emphasizes, the goal is not to make flood permanently “risk-free” for insurers. “Some companies see the value in flood but don’t want it on their balance sheet yet,” he noted. “If flood is going to become common, some insurers are going to have to retain the risk over time.”

In practice, that often means heavy quota share structures early on, paired with an expectation that insurers will gradually take on more exposure as confidence builds. “There isn’t a lack of flood capital,” Evans observed. “There’s a lack of insurers willing to make this a priority.” End-to-end reinsurance solutions can lower barriers to entry, but they cannot substitute for carrier commitment.

Despite this activity, the shape of growth remains telling. Much of the private flood market has expanded by serving risks that are already relatively well understood and economically attractive, such as homes exceeding NFIP coverage limits, properties near mapped floodplains, or policyholders reacting to premium increases. In many cases, private policies substitute for NFIP coverage rather than materially expanding the number of households insured. That dynamic was especially visible following Risk Rating 2.0, when pricing dislocations temporarily accelerated private-market growth before trends normalized.

The challenge facing private flood insurers today is therefore not underwriting or capital. Those problems are largely solved. The harder problem is scale — making flood insurance a routine purchase rather than a reactive one. That requires solving distribution: bringing coverage to the point of sale, aligning agent incentives, and rewarding market expansion rather than selective participation. The private flood sector will remain limited if it is built primarily on cherry-picking around the NFIP or grabbing growth when NFIP funding halts, as it did during the recent 2025 federal government shutdown. One that succeeds in broadening participation could begin to close the persistent gap between flood risk and flood coverage.

Flood insurance at the confluence

The NFIP was never meant to operate as a purely commercial insurer. Its mandate extends beyond risk transfer and into floodplain management, mitigation standards, and land-use signaling — an explicitly political choice to sustain communities in flood-prone areas. Private flood markets, by contrast, are built to price and select risk, not to regulate development or preserve broad access to coverage. Without a public backstop, underwriting and pricing would render large parts of the country effectively uninsurable. The result is that the NFIP and private flood are complementary rather than competing substitutes. The former provides baseline availability and policy structure, while the latter offers flexibility and capacity where underwriting confidence is strongest. The danger lies not in overlap, but in imbalance — where private insurers concentrate on economically attractive risks, while the NFIP increasingly absorbs the most difficult ones.

The U.S. flood insurance system is now approaching a genuine inflection point. The technical barriers that once constrained both public and private markets have largely fallen away. Risk is better measured, capital is available, and multiple operating models have proven viable. What remains unresolved are institutional choices about distribution, mandates, and risk sharing that will determine what kind of market ultimately emerges.

Broadly speaking, there are only a few plausible paths forward. One is continued drift: private flood grows largely through substitution, while the NFIP increasingly absorbs the most difficult risks and functions as a deeper residual market. Another is market-led expansion, in which bundling, embedded distribution, and carrier commitment make flood insurance routine in low- and moderate-risk areas, with the NFIP remaining central but less dominant. A third, more politically challenging path would involve changes to mandatory purchase or disclosure regimes that more explicitly treat flood as a shared household risk rather than an optional add-on.

None of these outcomes is preordained. But the direction taken will depend less on further modeling breakthroughs than on whether insurers, regulators, and policymakers can align around expanding participation rather than merely reallocating existing demand.

Regulators are already responding to this transition. State insurance departments and national bodies like NAIC have increased their attention, focusing on consumer clarity, solvency, accumulation risk, and model governance as more flood exposure moves outside the NFIP’s direct purview. The aim is not to slow innovation, but to place guardrails around a market that is still finding its footing.

Even with better oversight and better products, however, the central challenge remains unresolved: flood insurance is still treated as optional. It is rarely bundled with homeowners coverage, rarely presented clearly at the point of sale, and rarely revisited absent a lender mandate or recent loss. Mandatory purchase requirements, narrowly tied to SFHAs, capture only a fraction of today’s risk. Outside those zones, participation depends on individual initiative, an approach that has repeatedly failed to produce meaningful risk pooling. Until flood is treated as a core household risk rather than a specialty add-on, uninsured losses will continue to be borne largely by homeowners themselves.

Sources

- Congressional Research Service, Private Flood Insurance and the National Flood Insurance Program.

- NFIP’s Pricing Approach.

- NAIC 2025 Fall National Meeting Climate and Resiliency (EX) Task Force Meeting Slides.

- Jencap Flood Insurance Trends Approaching 2026.

- Insurance Information Institute, Spotlight on: Flood Insurance.

Developing News

The Rise (and Perils) of AI Summaries in Search Engine Results

he prevalence of AI-generated summaries within search engine results has increased dramatically over the past two years. An ongoing weekly study by Advanced Web Ranking showed that as of January 5th, 2026, Google’s search engine produced an AI Overview on 60.2% of queried keywords,1 compared to only 12.4% as of July 2024.2

But the rise in AI summaries does not necessarily coincide with an increase in the accuracy of the underlying large language models (LLMs). According to some sources, the latest models actually show an increase in “hallucinations,” a phenomenon in which the LLM inserts fabricated information into a response.3 Estimates for the frequency of these errors vary by model and query type. One ongoing study that looks at GenAI’s ability to summarize an article found hallucination rates between 1.8% and 7.8% per summary among the top GenAI models.4 Even Google’s Gemini model, when asked how trustworthy AI summaries are, provided this reply: “Recent tests in 2025 indicated that roughly one in five AI Overviews may return inaccurate or misleading answers. … Accuracy drops significantly for specific, less-documented topics where the AI may fill “data voids” with off-base information.”5

What’s troubling is not only the tendency of AI-generated information to be wrong, but its tendency to be “confidently wrong.” A study published in the Columbia Journalism Review6 in March 2025 found that eight leading GenAI tools had a collective error rate of 60% when providing citation information that could have otherwise been easily found by clicking through the first few search engine results. The incorrect responses were often presented with complete confidence and no qualifying statements or expressions of uncertainty. While the tools self-filtered by declining to provide responses in some cases, this behavior differed across the tools. ChatGPT, for example, provided a response to every query despite a high error rate in its responses. In contrast, Microsoft Copilot declined to reply for over half the questions.

What this means for actuaries:

Consider just a few possible ways that actuaries may rely on search engines to directly inform their work:

- Searching for laws/regulations ASOPs related to insurance pricing or reserving.

- Searching for information on actuarial methodologies or exam syllabi topics.

- Searching for information related to emerging sources of risk for purposes of risk classification or for assessing the possibility of adverse deviation of reserves.

Many of these use cases are related to niche, less-documented topics — the sorts of topics in which GenAI itself confesses that it is particularly error prone.

As a result, actuaries should be particularly careful when using AI summaries from search engines. While it can be tempting to rely on an authoritative-sounding AI summary instead of clicking into search results to read the details of a primary source (e.g., DOI bulletin, statutory law, ASOP, CAS paper, etc.), these AI summaries should at most be used as a starting point, not a final destination, for information. How would an actuary feel if Microsoft Excel would fabricate a result instead of correctly executing a formula 1% of the time?

- https://www.advancedwebranking.com/free-seo-tools/google-ai-overview#faq

- https://www.advancedwebranking.com/blog/ai-overview-study

- https://www.nytimes.com/2025/05/05/technology/ai-hallucinations-chatgpt-google.html

- https://github.com/vectara/hallucination-leaderboard

- Ironically, Gemini did not cite the source of the test results.

- https://www.cjr.org/tow_center/we-compared-eight-ai-search-engines-theyre-all-bad-at-citing-news.php

Developing News

Reviewing ‘Ash’umptions: Another Look at Volcanic Risk